You're probably in one of two spots right now.

Either you're building a fintech startup and somebody told you to apply to a fintech innovation lab because “that's how you get in front of banks.” Or you saw one of these programs online, read the glossy copy, and couldn't tell whether it was a real business opportunity or just corporate networking with better lighting.

I'm going to save you time. A good fintech innovation lab can help. A bad one is corporate theater. The difference is simple: does it get you into real conversations with people who can move your product through risk, compliance, procurement, and business-line ownership, or does it just give you mentor sessions and a demo day?

That's the whole game.

Your Guide to a Fintech Innovation Lab

You're building from a small office, a coworking desk, or your kitchen table. You have a product that makes sense to you. Then someone says, “You should look at a fintech innovation lab.” It sounds polished. Maybe too polished.

My blunt take: a fintech innovation lab is usually an introduction machine. It's less like school and more like a tightly managed broker between startups and large financial institutions.

That matters because banks, insurers, and asset managers don't buy software the way a fast-moving startup does. They don't wake up, like your pitch, and sign a contract by Friday. They move through committees, legal review, security review, internal politics, and budget ownership. If you don't already know how that machine works, you can waste a year talking to the wrong person.

A good lab shortens that learning curve. It gets you in the room with people who can tell you, fast, whether your product is viable for an enterprise buyer.

If fundraising is trying to get a warm intro to an investor, a fintech innovation lab is trying to get a warm intro to an institution. Same principle. Different buyer. Much harder sale.

If you're in Chicago or the Midwest, this kind of operator-to-operator access probably feels more useful than another loud networking event. That's why communities around founder connection, like Chicago Tech Week gatherings, often feel more honest than polished startup programming. The same filter applies here. You want access that leads somewhere.

A fintech innovation lab is worth your time when it helps you answer one hard question: will a regulated buyer actually use this?

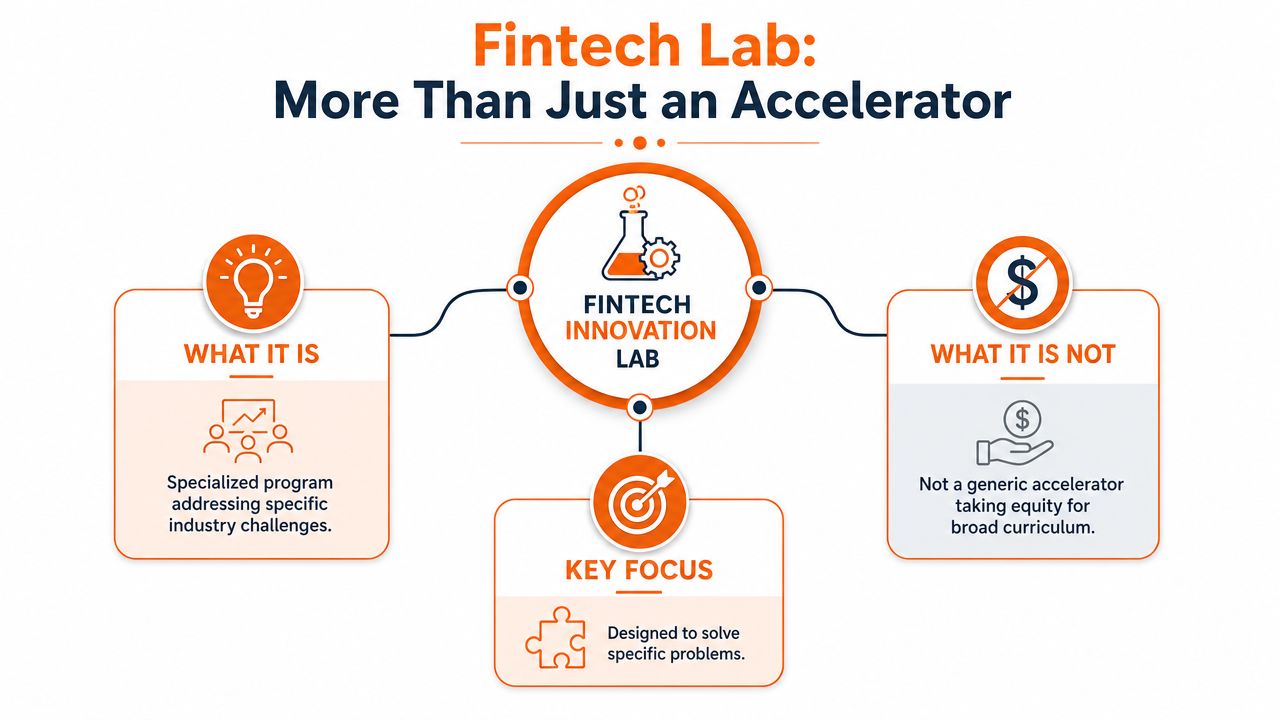

What a Fintech Lab Really Is and Is Not

Most founders misunderstand these programs at first. They hear “lab” and assume workshop, mentorship, curriculum, maybe some office hours. That's incomplete.

A fintech innovation lab is usually built to solve one ugly market problem: big financial institutions need innovation, but they're slow and risk-heavy. Startups move fast, but they lack trust, context, and access. The lab tries to bridge that gap.

What it is

The cleanest example is the New York FinTech Innovation Lab. It launched in 2010 through the Partnership for New York City and Accenture, and it runs as a 12-week intensive that connects startups with over 40 financial services and venture capital firms each year, according to Accenture's program announcement.

That setup tells you what the model really is. It's a structured bridge into institutions.

The best analogy is curated speed dating. On one side, you have banks, insurers, or other financial firms with specific operational pain. On the other, you have startups with a proposed fix. The lab screens both sides, creates the meetings, and keeps everyone focused on practical fit instead of random networking.

What it is not

It is not a generic startup accelerator with broad startup advice dressed up in fintech language.

If the program spends more time teaching generic pitch craft than forcing real enterprise feedback, I'd be skeptical. If the people you meet can't speak to security review, KYC or AML expectations, data governance, procurement friction, and internal ownership, it's probably not a real fintech lab in the useful sense.

That's why I tell founders to watch the wording. “Mentorship” is cheap. “Access to senior leaders inside financial institutions” is useful. Those are not the same thing.

If your product touches banking distribution, payments, or partner-led delivery, it also helps to have a working grasp of understanding embedded finance for banks before you walk into these conversations. You need to speak the buyer's language, not your product language.

Why the structure matters

The operating logic is simple:

- Tight time box keeps you from floating through endless coffee chats.

- Senior access helps you test against real decision criteria.

- Focused feedback reveals where your product breaks inside enterprise reality.

Here's the video version if you want another angle on the model.

Practical rule: If a lab can't tell you exactly who you'll meet and what those people can approve, challenge, or sponsor, assume the access is weaker than advertised.

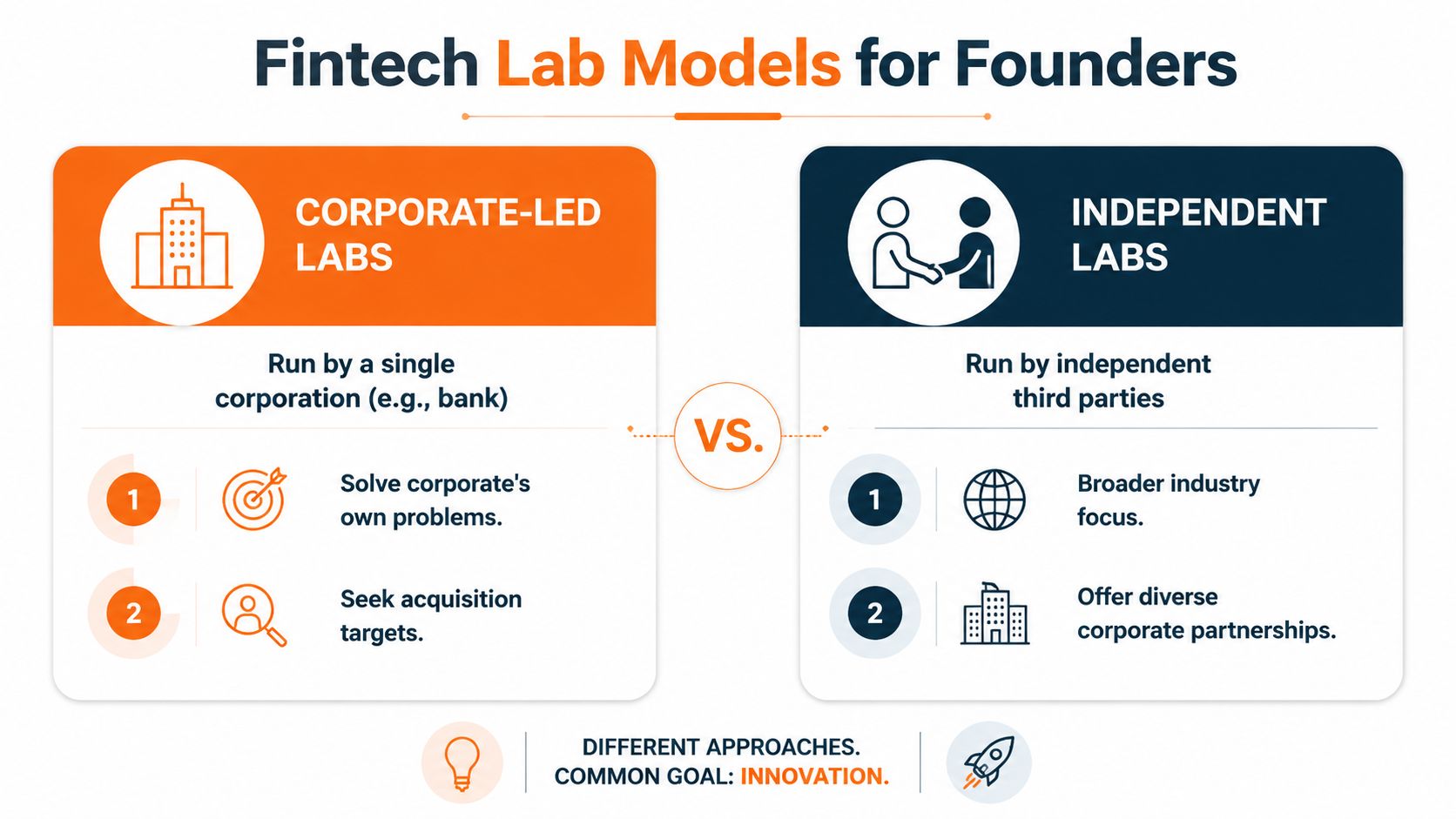

How Different Lab Models Work for Founders

Not all fintech labs are built for the same job. Founders get burned when they lump them together.

Some labs exist to help one corporation find solutions for its own problems. Some exist to create a broader market between multiple institutions and startups. Some want deep engagement. Some want light-touch validation. If you don't know which model you're entering, you can spend months chasing the wrong outcome.

Corporate-led labs

These are usually run by one bank, insurer, or large financial company.

The upside is focus. If your product cleanly solves that company's problem, you may get direct traction faster because everyone is looking at one buyer environment. The downside is concentration risk. You can leave with one relationship and no broader market learning.

This type is best when you already know your ideal customer profile and want one serious enterprise shot.

Independent or consortium-style labs

These tend to be run by third parties or ecosystem groups that connect startups with multiple financial institutions.

That usually gives you a wider sample of buyer behavior. You hear different objections, different compliance concerns, and different internal buying logic across several institutions. For early go-to-market learning, that's often stronger than going all-in on one corporate sponsor.

If you're still refining where your product fits, this model is usually safer.

Full-immersion versus part-time formats

This distinction gets ignored, but it matters a lot. Some founders can't disappear into a program for months. Others need a highly immersive environment to force progress.

A useful local example is the 1871 model. According to 1871's FinTech Innovation Lab page, that program runs as a 4-month engagement with a commitment of about 1 week per month. I like that format for founders who still need to run sales, shipping, product, and hiring at the same time.

Here's the founder filter I use:

| Lab model | Best for | Main risk |

|---|---|---|

| Corporate-led | Clear fit with one target buyer | You become too dependent on one institution |

| Independent | Broader market discovery | Meetings can stay broad if the program lacks teeth |

| Full-immersion | Big product or GTM reset | Time cost can hit the core business |

| Part-time | Operators who need flexibility | Easier to under-commit and drift |

If you're comparing local founder support options more broadly, this roundup of small business incubators is useful context. Just don't confuse incubators with fintech labs. An incubator helps you build a company. A fintech lab should help you sell into institutions.

Questions I'd ask before applying

- Who are the buyers? Name the institutions and the functions.

- What is the program trying to produce? Pilots, validation, partnerships, or PR.

- What does access look like? Group sessions are not the same as targeted working meetings.

- What happens after the cohort ends? If the answer is vague, that's a warning.

If the lab can't explain its buyer map in plain English, it probably doesn't have one.

The Real Benefits and Why You Might Join

Founders often pitch the wrong value of a fintech innovation lab. They talk about prestige. I don't care about prestige. I care about whether the program makes you more sellable to enterprise buyers.

That's the main upside.

Validation that actually matters

When a credible fintech lab selects you, investors and customers take a second look. That doesn't mean you've won. It means somebody with context decided you're worth evaluating.

In fintech, that matters because enterprise buyers are scared of wasting time. Any external filter that says “this startup is at least serious enough to review” helps.

Access to the people who can block or unblock a deal

You do not need more random intros. You need targeted feedback from the exact people who can tell you why your product won't survive enterprise review.

That usually means some mix of business-line leaders, innovation teams, compliance, security, legal, and procurement. Founders hate hearing “your architecture won't pass review” or “your data handling makes this impossible,” but hearing it early is a gift.

If you're building infrastructure or regulated workflows, your prep should include a realistic plan for building secure fintech software. Labs are useful partly because they expose security and integration weaknesses before a long sales cycle buries you.

A stronger fundraising story

The New York program has supported 130 startups that have raised $3 billion in global capital, and in 2021 it received more than 200 applications from around the world and selected 10 companies, according to this program summary.

I wouldn't read that as magic. I'd read it as a signal.

Founders who survive a serious lab process usually come out sharper. Their value proposition is tighter. Their enterprise objections are more mature. Their roadmap makes more sense to regulated buyers. That improves the fundraising narrative because the company looks less like a speculative concept and more like a business that understands how real customers buy.

When you should skip it

A fintech innovation lab is a bad use of time if:

- You're too early and can't demo anything real.

- Your buyer isn't institutional and you're forcing a fintech wrapper onto a non-fintech business.

- You want distribution but hate feedback from enterprise stakeholders.

- You need revenue immediately and can't afford slow-cycle relationship building.

Don't join a lab because you want the logo wall. Join because you want your GTM assumptions stress-tested by the people who can break the deal.

Finding the Right Lab From Chicago to Global

Most founders evaluate fintech labs backward. They start with brand name, city, or prestige. I start with one simpler question: what commercial motion is this lab likely to create?

That cuts through a lot of noise.

Chicago is a good example of why format matters

For founders in the Midwest, the local advantage isn't hype. It's practicality.

Chicago's 1871 version has a cadence that can fit around the reality of building. You can keep running the company while still getting structured feedback. I like that because many early founders don't need another full-time program. They need disciplined exposure to the right people and enough pressure to refine their offer.

The question most founders fail to ask

The public story around labs usually sounds the same: mentors, access, validation, community, demo day, maybe alumni fundraising. Fine. But that still leaves the most important issue unanswered.

According to the New York program's own public framing, a real open question is whether a lab helps startups reach commercial traction or mostly produces demos and networking. The program notes that public descriptions rarely quantify conversion to paid pilots or procurement, which makes comparison hard even when aggregate fundraising numbers look strong, as described in the New York application page for the 2026 class.

That's exactly right. I care much less about polished alumni slides than I do about whether founders left with real buying momentum.

How I'd evaluate any lab

Use this checklist before you apply:

- Ask for buyer specificity. Which institutions participate, and from which functions?

- Ask for workflow detail. Do you get targeted problem-solving sessions, or mostly broad panels?

- Ask about post-program continuity. Are there follow-on introductions, pilot pathways, or internal champions?

- Ask alumni what changed. Did the lab alter pricing, product scope, security posture, or sales motion?

- Ask what happened after the applause. Demo day is theater unless it creates working next steps.

If you need a broad scan of startup-friendly vendors and categories while shaping your stack, this list of fintech solutions for startups can help frame what buyers may already be seeing in the market. That context matters when you position your product.

And if you're searching locally for founder infrastructure outside formal lab programs, a guide to incubator options near you can help you compare support environments. Just keep the distinction clean. Community support and enterprise access are different tools.

A lab earns its keep when it changes your odds of landing a real institutional customer. Anything less is just a nicer calendar.

Getting In and Replicating the Benefits

Getting into a fintech innovation lab is less about polish and more about fit. Most founders think they need a prettier deck. Usually they need a sharper answer to one question: why will a regulated institution care right now?

That answer has to be concrete.

How I'd prepare the application

Start with the problem, not the product. Show that you understand the workflow you're entering.

A weak application says, “We use AI to modernize compliance.” A stronger one says, “We reduce review friction in a specific compliance workflow, and we know exactly where legal, risk, and operations will challenge adoption.”

Use this sequence:

- Name the buyer clearly. Bank, insurer, lender, broker, or asset manager.

- Name the pain precisely. Not “inefficiency.” Real friction in an actual workflow.

- Show why now. Regulatory pressure, staffing burden, cost of manual review, or integration pain.

- Prove your team can execute. Labs care whether you can survive enterprise complexity.

- State what you need from the lab. Intros, product validation, pricing feedback, pilot design, compliance input.

How to stand out once you're in

Most founders waste the program by acting like students. Don't.

Treat every session like deal progression. Walk in with hypotheses. Walk out with revised language, objection handling, and next questions. If someone from a bank gives you a vague compliment, ignore it. If they tell you your onboarding process would die in procurement, write that down and fix it.

A few habits help:

- Bring a tight demo. Show the workflow, not the feature dump.

- Track objections. If three institutions raise the same concern, that is your roadmap.

- Ask ugly questions. Security, implementation burden, internal sponsor risk, budget ownership.

- Follow up fast. Enterprise people forget startups that drift.

If you don't get in

This matters more than people admit. You do not need formal acceptance to get most of the value.

You can build your own version of a fintech innovation lab by creating a small system around yourself:

- A founder circle that gives blunt product and GTM feedback

- A few domain mentors from compliance, banking operations, or enterprise sales

- A target account list with disciplined outreach

- A learning loop where every call changes your pitch, demo, or roadmap

That homemade version lacks brand polish, but it can still work. In some cases, it works better because you control the buyer list and the pace.

What you can't fake is honesty. The reason good labs help is not the logo. It's the forced contact with reality. You can create that yourself if you're willing to hear “no,” “this won't pass,” and “you're solving the wrong layer of the problem” often enough.

If you're a Chicago or Midwest founder who wants the honest version of startup support, Chicago Brandstarters is worth a look. It's a free vetted community for kind, hard-working builders who want real conversations, small private dinners, and practical feedback instead of performative networking. If you're trying to build with more truth and less noise, that's the right room.

Leave a Reply