Most advice about financial planning for startups is built for companies chasing venture rounds, not for the founder in Chicago, Milwaukee, Indianapolis, or Des Moines trying to sell real products at a profit. That advice tells you to dream in funding milestones. I think that's backwards.

If you're building a bootstrapped or lightly funded ecommerce brand, your first job isn't to impress investors. It's to stay alive long enough to learn what customers want, fix your pricing, and stop leaking cash. Fancy models won't save you if your bank balance is lying to you.

I've watched founders obsess over decks, logos, and growth stories while ignoring the boring math that decides whether they make it to next spring. The math wins every time.

Why Most Financial Advice for Startups Is Garbage

Most startup finance content is written for a tiny club. It assumes you're raising big rounds, hiring fast, and building software. That's not your world if you're testing a product line from your apartment, managing small inventory buys, and trying to grow without lighting money on fire.

For Midwest product founders, the fight is simpler and harder. You need enough cash to buy inventory, pay vendors, cover software, survive slow months, and still have room to fix mistakes. That's financial planning for startups in practice.

Most founders don't die from bad ideas

They die from bad cash habits.

A U.S. Bank finding summarized here says 82% of small businesses that failed did so because of poor cash flow management. That's the stat I want burned into your brain. Your product can be good. Your customers can like you. You can still lose because you ran out of money before the business had time to work.

Practical rule: If you don't know your cash position, your monthly burn, and your next ugly expense, you're not running a business. You're gambling.

The popular advice also skips the data plumbing behind clean decisions. Once your orders, ad spend, returns, and channel data start living in five different tools, you need a simple system for seeing reality. If you want a plain-English primer on that side of the stack, read this guide to modern data warehouse architecture. You don't need to become a data engineer. You do need numbers you can trust.

The VC script hurts bootstrapped founders

Here's the script you should ignore:

- Raise first: Build the story before you build the business.

- Hire early: Add people before you lock in demand.

- Scale ads fast: Spend more because growth feels good.

- Model big exits: Pretend future size solves present sloppiness.

That's nonsense for a revenue-light brand.

You need a tighter script:

- Get your pricing right

- Protect margin

- Buy inventory carefully

- Track cash weekly

- Earn the right to spend more

If you want a good example of thinking against startup groupthink, read these contrarian founder reviews. Most founders need less theater and more discipline.

My bias is simple

I care more about survival than startup cosplay.

If you're bootstrapping, a simple honest plan beats a beautiful fantasy. I'd rather see a founder who knows their reorder risk, refund drag, and true margin than one who can talk for an hour about TAM and brand vision.

That's the frame for everything below.

Your One-Page Financial Model

Your first model should fit on one page. If it takes fifty tabs to explain your business, you don't understand your business yet.

It's like your car dashboard. You don't need to see the engine block while driving. You need a few gauges that tell you if you're safe, drifting, or about to stall.

What goes on the page

Your one-page model needs these lines:

| Line item | What it means | Why I care |

|---|---|---|

| Revenue | Money collected from sales | Tells me whether demand is real |

| COGS | Product and fulfillment costs | Shows whether each sale helps or hurts |

| Gross margin | Revenue minus COGS | Gives room to operate |

| Operating expenses | Software, contractors, rent, ads, admin | Shows the cost of staying open |

| Net profit or loss | What's left after all expenses | Tells me if the model works |

| Cash on hand | Actual money in the bank | Keeps fantasy out of the spreadsheet |

Keep it ugly if needed. Google Sheets is fine. The tool doesn't matter. Clarity matters.

Build it from the ground up

Don't start with a giant annual revenue number and work backward. Start with what you can sell.

A good model begins with units. The best practice is to build a bottom-up model for the first 1 to 2 years based on real drivers like units sold, then use a top-down model for years 3 to 5 based on market share, as explained in J.P. Morgan's guide to financial planning for entrepreneurs and founders.

Here's how I do it:

- Start with units sold: How many orders can you realistically produce and ship?

- Then price: What do customers pay after discounts?

- Then returns and refunds: Ecommerce founders forget this all the time.

- Then costs: Product, packaging, shipping, platform fees, and ad spend.

- Then timing: When does cash leave, and when does it come back?

A spreadsheet should answer one blunt question: if you sell what you think you'll sell, does cash go up or down?

If you need help framing the business before the numbers, use a business model canvas template. It helps you tie the math to the actual business model instead of making up disconnected assumptions.

Use three scenarios

I don't trust single-track forecasts. They're bedtime stories.

Run three cases:

Best case

Your launch lands, conversion is healthy, returns are manageable, and your repeat purchase behavior looks better than expected.

Most likely

This is your working plan. Keep it boring. Boring is good. Boring means you can make decisions without lying to yourself.

Worst case

Ads cost more. Your supplier is late. Customers buy slower. A batch has defects. This scenario is not pessimism. It's professionalism.

A one-page model with three columns beats a giant spreadsheet nobody updates.

What founders usually miss

Bootstrapped product brands miss the same stuff over and over:

- Packaging creep: Boxes, inserts, labels, and tape add up.

- Small subscriptions: Shopify apps, email tools, and random SaaS nibble you to death.

- Founder pay: If you never budget your own compensation, your model is fake.

- Inventory mistakes: Buying too deep too early freezes cash.

- Discount addiction: Revenue rises while margin erodes.

Financial planning for startups isn't about predicting the future perfectly. It's about forcing honesty into your decisions. When the model is short, visible, and updated, you'll use it.

Master Your Cash Flow and Burn Rate

I once watched a founder celebrate a strong sales month while dodging vendor emails. Revenue looked fine. Cash was a mess. They had paid for inventory, ads, and packaging before the money from sales had fully landed. On paper, things looked alive. In the bank account, they were choking.

That's why I care more about cash flow than vanity growth.

Know your burn or get burned

Net burn is what you lose each month after revenue offsets expenses. Runway is how long your current cash lasts at that pace.

A simple runway formula is this: divide cash on hand by net burn. Ramp gives a clean example in its startup planning guide: if you have $300,000 in cash and a $50,000 monthly net burn, you have 6 months of runway according to this runway calculation example.

That number is not trivia. It's a deadline.

My operating rule

I want founders to know three things every week:

| Question | What you need |

|---|---|

| How much cash do I have? | Real bank balance |

| What am I burning? | Monthly net burn |

| How long can I survive? | Runway in months |

If you can't answer those in under a minute, your financial system is too loose.

For founders trying to understand how runway connects to funding choices, this guide to startup funding is worth reading. Use it as context, not as permission to raise before you've cleaned up your operating mess.

Cash flow problems hide in timing

A product brand can sell well and still get trapped because cash moves on a different schedule than profit.

Common traps:

- Inventory upfront: You pay before the item earns a dollar.

- Ad spend now: Meta and Google don't wait for your customers to pay off your credit card.

- Retail terms later: Wholesale money can crawl in long after goods ship.

- Returns fast: Refunds leave your account before replacement sales catch up.

That's why I tell founders to track a weekly cash calendar, not just a monthly P&L. Your accountant may care about clean books at month end. You need to care about whether payroll, inventory, and software hit before the next cash inflow.

Cash flow is timing. Timing is survival.

If you want a deeper operating checklist, read this practical guide to cash flow management for small business.

Add the buffer you don't want to add

Founders almost always undercount expenses. Always.

Good practice from banking and small-business guidance is to add an explicit contingency buffer of roughly 15 to 20% on top of projected expenses, especially for stuff like fulfillment, software, and customer support tools. I agree with that completely. I call it the "oh crap" line.

Make a row in your model for it. Don't bury it.

Here are the places that usually blow up first:

- Freight and shipping surprises

- Rush production fees

- Subscription bloat

- Returns processing

- Customer service labor during a launch

You also need to reforecast when reality changes. New supplier quote? Update the sheet. Bad launch week? Update the sheet. Big retailer asks for terms? Update the sheet.

A short video can help if you want a refresher on founder-friendly finance basics:

Financial planning for startups gets real when you stop asking, "How much can I grow?" and start asking, "How many bad months can I absorb before I lose control?"

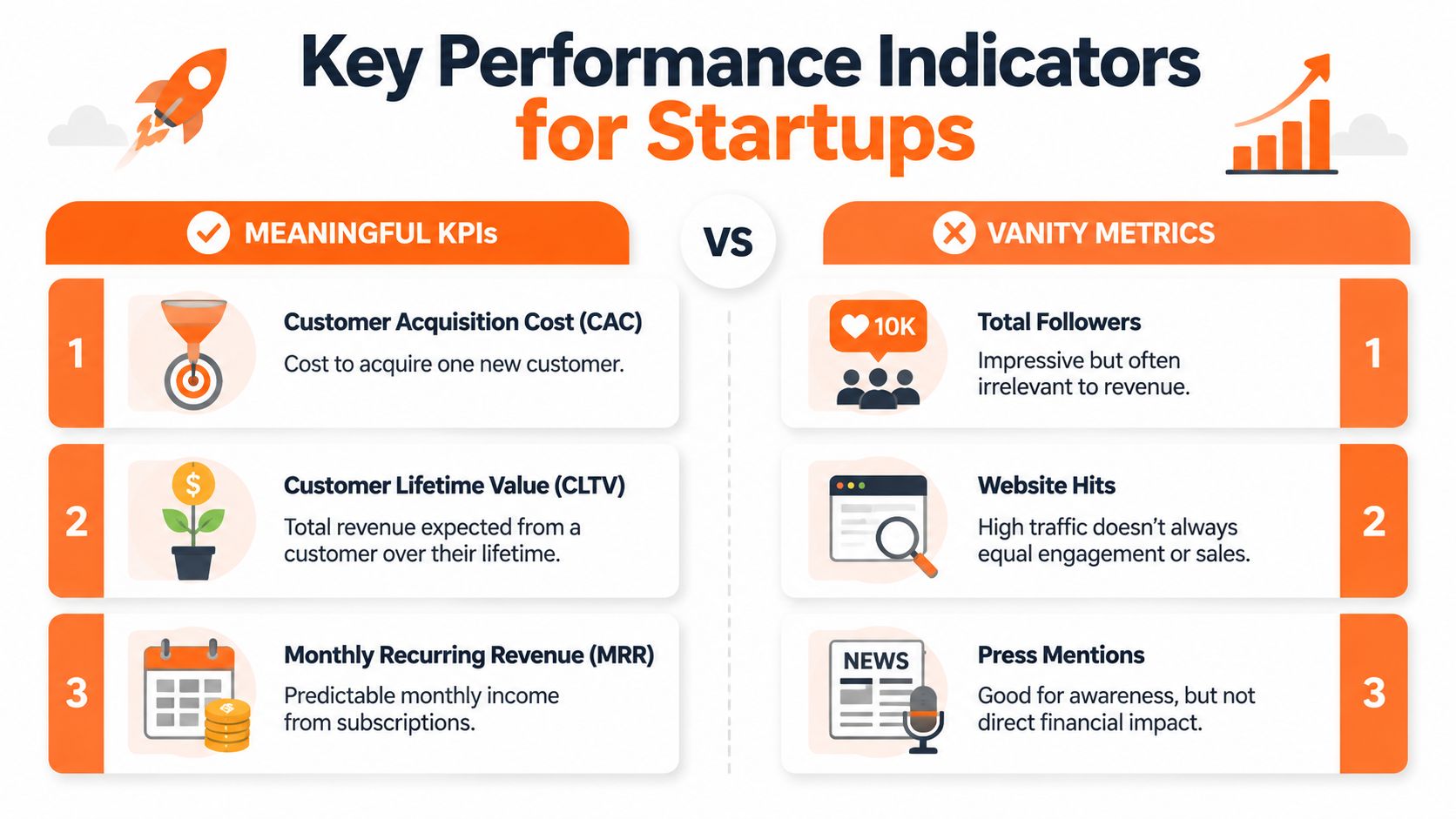

The Only KPIs That Actually Matter

Most early founders track nonsense. Followers. Reach. Site traffic. Likes. Open rates without purchase behavior. None of that pays your supplier.

For an early-stage ecommerce brand, I care about unit economics. I want to know whether each customer and each order makes the business stronger or weaker.

The three numbers I want first

You do not need a giant KPI dashboard. You need these:

CAC

Customer acquisition cost is what you spend to get one new customer. If you spend money on Meta ads, creators, samples, and promotions, that spend has to tie back to actual customers acquired.

LTV

Lifetime value is the gross profit a customer creates across their relationship with your brand. If people buy once and disappear, your LTV is weak no matter how good your social media looks.

Contribution margin

This is sale price minus the variable costs required to make and sell that item. If you don't know contribution margin by SKU, you're making decisions in the dark.

Why this matters more than "growth"

A founder can grow revenue and still train the business to lose money faster.

If your CAC is sloppy, your LTV is soft, and your contribution margin is thin, more sales can make your problems worse. That's the ugly truth a lot of startup content avoids because "growth" sounds sexier than "fix your gross margin."

A 2025 survey cited in J.P. Morgan's founder planning content said 61% of early-stage ecommerce founders had no formal unit-economics spreadsheet, and only 19% could confidently calculate contribution margin per SKU. I believe it, because I keep meeting founders who know their follower count better than their best product's margin.

Reality check: If you can't calculate contribution margin on your top SKU, pause your marketing experiments until you can.

What I ignore on purpose

Here are metrics I push down the priority list for very early brands:

- Total followers: Nice for ego. Weak for planning.

- Raw website sessions: Traffic without conversion tells me little.

- Press mentions: Attention is not cash.

- Email list size: A list can be dead weight if nobody buys.

I don't mean these are useless forever. I mean they are secondary until the business proves that each sale has economic sense.

A quick scorecard

Use a plain-English review each month:

| Metric | Healthy question |

|---|---|

| CAC | Did it get cheaper, or did we buy customers badly? |

| LTV | Do people come back enough to justify acquisition spend? |

| Contribution margin | Does each product sale create room to operate? |

If one of those breaks, stop acting like the answer is "more marketing."

Financial planning for startups gets easier once you stop drowning in metrics and focus on the few that expose whether the machine works.

Planning to Raise Money or Not

You do not need to raise money just because startup culture says you should. A profitable, controlled business is a serious win. I wish more founders treated bootstrapping as a power move instead of a consolation prize.

Money is a tool. It is not proof that the business is good.

Raise for speed, not rescue

I only like fundraising when the business already has signs of life. Clear demand. Working unit economics. A model that shows where the money goes. A founder who knows what happens if revenue slips or costs rise.

If you're raising because you're disorganized, investors won't save you. They'll just make the consequences bigger.

Here is the split I use:

- Bootstrap when you can grow through cash flow, controlled inventory, and disciplined testing.

- Raise when added capital would let you press an already working advantage.

- Wait when the economics are still fuzzy and you'd only spend the money learning basic lessons.

Strong planning gives you options

The founders with influence are the ones who can choose.

They can keep bootstrapping because the business isn't starving. They can raise because they can explain the model cleanly. They can say no to bad terms because they aren't desperate.

That's why the earlier work matters. One-page model. Scenario planning. Tight cash tracking. Real unit economics.

A source cited by DXA Group says founders who present detailed financial models, unit economics, and scenario analyses improve their chances of moving from pitch to term sheet by an estimated 20 to 30% in this discussion of the importance of financial planning for startups.

That's useful. But don't twist it into "therefore I must raise." The lesson is simpler. Knowing your numbers improves your position, whatever path you take.

Raise money to make a good machine go faster. Don't raise money to hide that the machine rattles.

What I want to hear from a founder

If you do decide to raise, I want your answers to sound like this:

| Question | Strong answer |

|---|---|

| Why this capital? | "To fund proven demand, inventory, and measured channel expansion." |

| What changes if sales slow? | "We already modeled the downside and know where to cut." |

| How do you make money? | "Here are our unit economics by product and channel." |

That level of control changes the conversation. It also protects you from lying to yourself.

Get Your House in Order Next Steps

This part feels boring. It's also where a lot of founders save themselves from future pain.

If your finances are messy, every decision gets harder. You hesitate on inventory. You misread profitability. Tax season turns into a horror movie. Clean basics fix more than people think.

Do these this week

Start with the unglamorous stuff:

- Open a separate business bank account: Mixing personal and business spending wrecks visibility.

- Pick one accounting system: Keep it simple and consistent. A basic setup is better than chaos in five tools.

- Track cash weekly: Not when you're stressed. Every week.

- Save receipts and categorize expenses: Future you will be grateful.

- Find a local accountant early: Good help before the emergency is cheaper than bad help during one.

Keep the process light

Don't build a finance department for a tiny brand. Build a rhythm.

I like this monthly cadence:

- Update actual sales and expenses

- Review cash on hand

- Compare results to your one-page model

- Adjust the next few months, not your fantasy five years from now

Small clean habits beat heroic cleanups.

The point of financial planning for startups isn't to look impressive. It's to make better decisions while you still have time to act. Keep the model short. Keep the books clean. Keep your eyes on cash. That's how you give a good business a real chance.

If you're a kind, ambitious Midwest founder who wants honest feedback, real operator war stories, and a room full of builders who care more about substance than posturing, join Chicago Brandstarters. It's a free community for Chicagoans and Midwesterners building brands from idea stage to seven figures, with small private dinners and a vetted group chat built for people who want to help each other win.

Leave a Reply