You're probably doing what most early founders do. You check sales, stare at your bank balance, maybe look at ad spend, then hope the rest is fine.

That works for a while. Then inventory piles up, a supplier wants payment, a loan hits your account, and suddenly you realize you don't know what your business owns, what it owes, or how fragile the whole thing is.

That's where a balance sheet helps. I don't mean as an accounting exercise. I mean as a decision tool.

If you want to learn how to read a balance sheet, start with one mindset shift. This document isn't judging you. It's showing you the physical structure of your business at one moment in time. It's an x-ray for your business. It won't tell you everything, but it will tell you whether the bones are straight, cracked, or under too much pressure.

Your Financial X-Ray Not a Report Card

A balance sheet is a snapshot. One date. One frame. It shows assets, liabilities, and equity.

If that sounds abstract, use the house example. You buy a house. The house is the asset. The mortgage is the liability. The part you own is the equity. Business works the same way.

What the snapshot actually tells you

When I look at a founder's balance sheet, I'm asking simple questions:

- How much cash is real cash?

- How much of the business is funded by debt?

- Is inventory helping or trapping cash?

- If bills hit this month, can the company handle it?

That's it. No finance theater.

A bad balance sheet usually shows up in your stress before it shows up in your bookkeeping.

This is why I tell founders to stop treating the balance sheet like a tax-season artifact. Read it monthly. If you're rusty, these Professional Careers Training financial insights are a solid extra primer alongside your own books.

Why transparency matters

Balance sheets matter most when people ignore them. Enron's 2001 collapse made that painfully clear. The company hid $13 billion in debt using off-balance-sheet entities, and the fallout helped drive stricter disclosure rules under the Sarbanes-Oxley Act of 2002, as explained in Fidelity's overview of what a balance sheet is.

For you, the lesson is simpler. Don't hide from the numbers in your own business.

If your cash position is tight, face it. If your liabilities are creeping up, face that too. If you need a cleaner way to connect this to day-to-day money decisions, pair your balance sheet with a practical guide to cash flow management for small business.

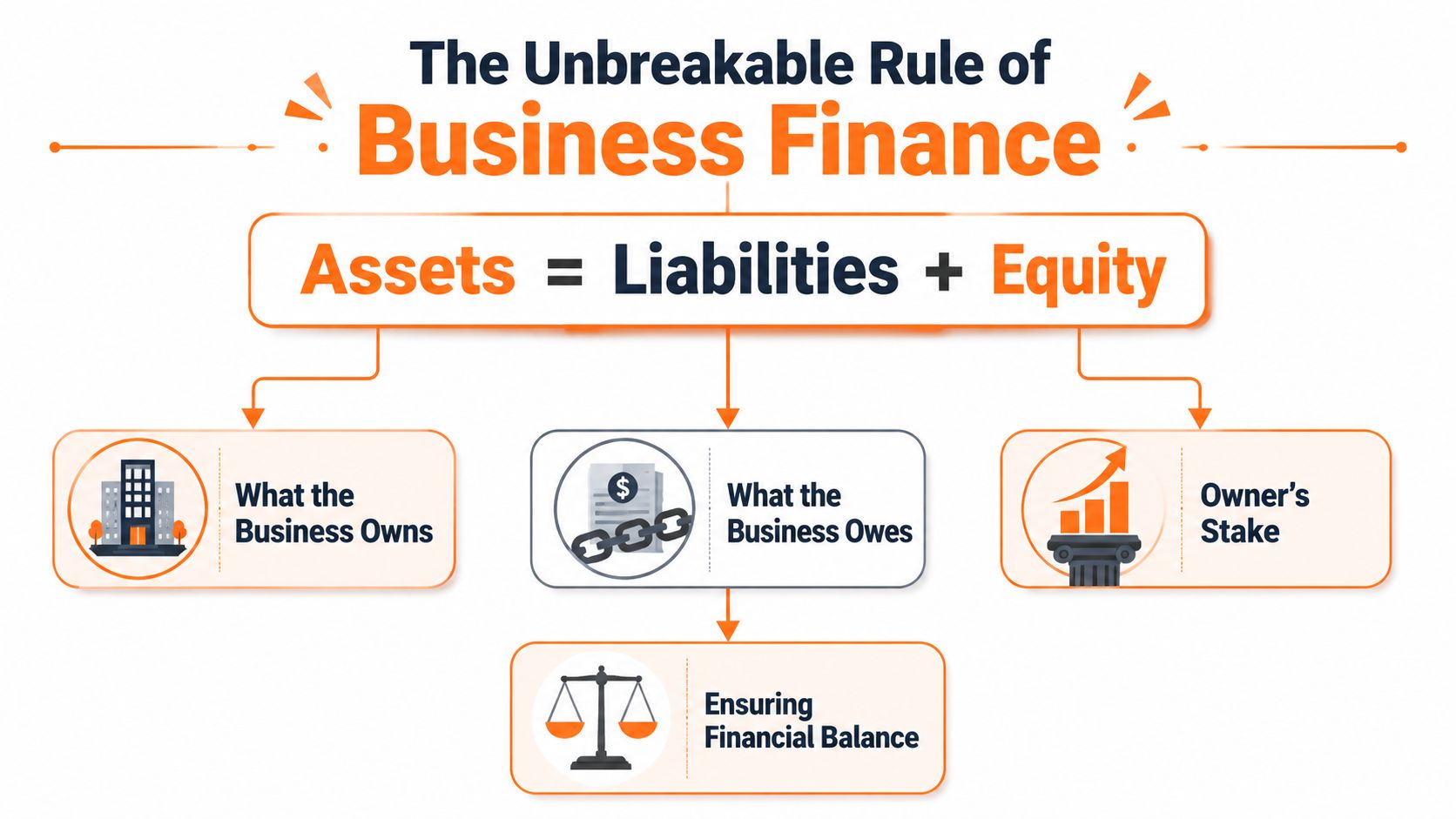

The Unbreakable Rule of Business Finance

Everything comes back to one line:

Assets = Liabilities + Equity

That equation comes from the double-entry accounting system formalized by Luca Pacioli in 1494 in Summa de arithmetica, and it still anchors modern financial reporting, as noted in this explanation of how to read a balance sheet.

The house analogy still wins

Forget accounting jargon for a minute.

Say you buy a house worth $100,000. You owe $44,000 on the mortgage. Your ownership stake is $60,000. The numbers must balance.

| Part | Amount |

|---|---|

| Asset value | $100,000 |

| Liability | $44,000 |

| Equity | $60,000 |

That's the whole game.

A business balance sheet is the same structure:

- Assets are what your business owns

- Liabilities are what your business owes

- Equity is what belongs to you after debt

What this looks like for an early founder

For a small ecommerce brand, the pieces are easy to picture:

- Assets might include cash, inventory, receivables, a laptop, or packaging supplies.

- Liabilities might include supplier bills, credit card balances, or a Shopify Capital advance.

- Equity starts with the cash you put in and grows when you keep profits in the business.

Here's the important part. Every transaction touches at least two parts of the equation.

You put money into the business. Cash goes up, equity goes up.

You buy inventory with a card. Inventory goes up, liabilities go up.

You repay debt. Cash goes down, liabilities go down.

Practical rule: If you can explain what changed in two places, you already understand more accounting than most founders think they do.

Don't overcomplicate the first read

You do not need to memorize textbook categories to get value from this. I'd rather you understand the structure cold than recite definitions badly.

If you want another plain-English walkthrough after this, MyOfficeOps has a clean guide on how to read a balance sheet. Use it to reinforce the basics, then come back to your own numbers.

Your Company's DNA Assets Liabilities and Equity

A founder at the idea stage usually asks me the same thing. “What if my balance sheet is tiny?”

Good. Tiny is fine. Messy is the problem.

Your balance sheet is your company's DNA. Even before big revenue shows up, it tells me how you're building. Are you funding the business with your own cash? With debt? With supplier terms? Are you tying cash up in products too early? Are you carrying obligations you can't support yet?

Assets are the fuel and the tools

Start at the top of the asset side and read it like you're standing over your own shoulder.

Cash is your oxygen. It buys you time.

Accounts receivable is money customers owe you. It counts, but it isn't cash yet.

Inventory is cash wearing a costume. It only becomes useful when it sells.

Equipment is the stuff you use for longer than a year, like a laptop, camera, or printer.

I usually divide assets into two buckets:

| Type | What it means |

|---|---|

| Current assets | You can turn them into cash within a year |

| Non-current assets | You expect to hold them longer |

For product brands, founders get fooled by inventory all the time. They see shelves full of units and feel rich. Then rent, ads, and supplier payments hit, and they realize their “asset” can't pay today's bills.

That's why carrying too much stock is dangerous. If inventory decisions are getting sloppy, tighten them up and learn the true cost of holding products with this guide to inventory carrying cost.

Liabilities are promises you already made

Liabilities are simpler than people think. They're just obligations.

Maybe you owe a factory. Maybe you owe American Express. Maybe you took a short-term working capital loan. Maybe sales tax is sitting there waiting to be paid.

Current liabilities come due soon. Long-term liabilities come due later. I care more about the timing than the label. A small business dies faster from short-term pressure than from a long-term note with manageable payments.

Equity is what you've actually built

Equity is the part founders misunderstand most.

If you put in cash to start the business, that starts equity. If the business earns money and leaves it inside the company, that also builds equity through retained earnings. If losses pile up, equity shrinks.

Here's the blunt version. Equity is your cushion. It's the part of the business that belongs to you after everyone else gets paid.

If liabilities eat the whole asset side, you don't own much. You're renting your business from your creditors.

The one number I want you to watch early

For an early-stage founder, working capital matters fast. It is current assets minus current liabilities.

Positive working capital gives you room to operate. Negative working capital means short-term stress. Financial health studies cited by Fidelity noted that 35% of startups in 2022 had negative working capital, which is one reason so many young companies feel busy but cash-starved.

If your numbers are still small, that's fine. Build the habit now. A one-page balance sheet with clean categories beats a bigger business with sloppy books every time.

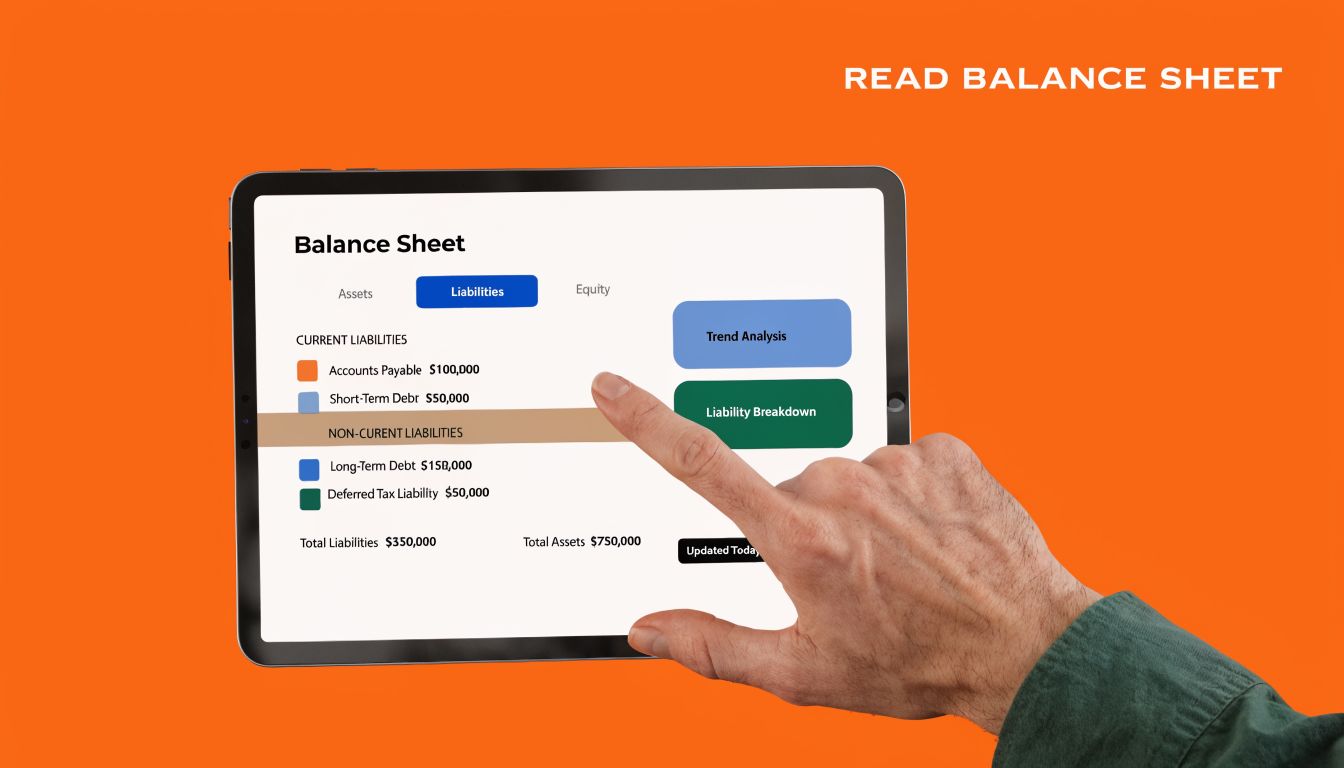

Let's Read a Real Balance Sheet Together

Let's use a simple ecommerce example. Nothing fancy. Just enough to see the story.

A stripped-down example

Here's the balance sheet:

| Line item | Amount |

|---|---|

| Cash | $20,000 |

| Accounts receivable | $5,000 |

| Inventory | $30,000 |

| Total assets | $55,000 |

| Accounts payable | $15,000 |

| Short-term loan | $10,000 |

| Total liabilities | $25,000 |

| Common stock | $1,000 |

| Retained earnings | $29,000 |

| Total equity | $30,000 |

Assets equal liabilities plus equity. $55,000 = $25,000 + $30,000. Good.

Now read the story, not just the math.

You've got $20,000 in cash. Fine.

You've got $30,000 in inventory. That means more capital is trapped in products than sitting in the bank. That's not automatically bad, but it is a warning to pay attention.

You owe suppliers $15,000 and owe another $10,000 on short-term debt. So pressure is coming from both vendors and lenders.

What jumps out first

The first thing I'd say over coffee is this: your business can survive short-term obligations on paper, but too much of your safety sits in inventory.

That matters because inventory doesn't always convert to cash on your schedule. It converts on the customer's schedule.

Here's where founders get confused. They think profit solves this. Sometimes it doesn't. You can show a profit and still be squeezed because cash is parked in stock or receivables. That's why I always read the balance sheet next to the P&L. If you need help making that connection, this guide on how to format income statement gives you the other half of the picture.

The three reads I'd make

Liquidity read

Can this company pay what's due soon without panic?Inventory read

Is product serving the business, or is the business serving product?Owner strength read

Is the founder building from retained earnings, or leaning too hard on borrowed money?

A balance sheet gets useful when you stop asking “What does this term mean?” and start asking “What does this force me to do next?”

If you want a quick visual walkthrough before building your own reading habit, this short video is useful:

What I'd do if this were my company

I wouldn't celebrate the balanced equation. That's table stakes.

I'd ask whether the inventory is moving fast enough, whether the receivables are aging cleanly, and whether the short-term loan is buying productive growth or just plugging holes. If the loan is covering old mistakes, I'd cut spend and fix operations. If it's funding fast-moving inventory with reliable margins, I'd watch it closely but stay calm.

That's how to read a balance sheet like an operator. You're not admiring the form. You're deciding what to do Monday morning.

The Only Financial Ratios You Need to Track

Founders love to over-measure. Don't.

If you're early, you do not need a dashboard with fifteen ratios and rainbow charts. You need a short list that changes behavior. I'd track four.

Current ratio

Current ratio = Current assets / Current liabilities

Using the example above:

$55,000 / $25,000 = 2.2

That tells me the company can cover near-term obligations with near-term assets.

A practical range people often watch is 1.5 to 2.0. Once you slide too close to the line, life gets tight fast. A Coursera summary of balance sheet analysis cites a 2019 Deloitte benchmark showing companies with current ratios in the 1.1–1.4 band had 1.8 times higher probability of liquidity stress than peers above 1.6.

If your current ratio is drifting toward that danger zone, don't wait. Cut purchase orders. Slow hiring. Push customers to pay faster. Renegotiate supplier terms.

Quick ratio

Quick ratio = (Cash + equivalents + receivables) / Current liabilities

This ratio strips out inventory. Good. Inventory is usually the liar in the room.

In the verified example, $50,000 of liquid assets against $30,000 of current liabilities gives a quick ratio of 1.67. That's a cleaner test of whether the business can handle short-term pressure without needing to sell stock first.

If your current ratio looks fine but your quick ratio looks weak, your liquidity is thinner than you think.

Debt-to-equity ratio

Debt-to-equity = Total liabilities / Total equity

In our sample:

$25,000 / $30,000 = 0.83

That tells you how much of the business is financed by outsiders versus owners.

I like this ratio because it cuts through founder optimism. If debt is climbing faster than equity, you are borrowing confidence from the future. Warren Buffett's rule of thumb is to prefer liabilities no more than 0.8× equity, and the example of $44,000 in liabilities against $60,000 in equity produces 0.73, which passes that test.

Working capital

Working capital = Current assets – Current liabilities

This is the simplest one and often the most useful.

Positive working capital means you have room. Negative working capital means every surprise hurts. If I'm advising a pre-revenue founder, I care about this more than most vanity metrics.

My rule: If one ratio forces a hard conversation, that ratio is doing its job.

Use ratios to make decisions, not to sound smart

Here's the short playbook:

- If current ratio is weak: preserve cash now

- If quick ratio is weak: stop trusting inventory to save you

- If debt-to-equity is rising: stop financing losses with debt

- If working capital is negative: shorten the time between spending cash and collecting cash

If you want help turning raw statements into something easier to scan, a tool like this financial performance analyzer can help you organize what you already have. Just don't confuse analysis with action. A prettier report won't fix a bad purchasing decision.

Balance Sheet Red Flags and How to Fix Them

I don't use a balance sheet to admire the past. I use it to catch problems before they punch me in the face.

Red flag one is inventory creep

If inventory keeps growing while cash gets tighter, your business is buying hope. That's dangerous.

Fix it fast:

- Cut the next order: Don't reorder because the spreadsheet says you used to.

- Move stale units: Bundle, discount, or kill SKUs that aren't earning their shelf space.

- Buy narrower: Fewer winners beat a warehouse of maybes.

Red flag two is receivables that look bigger every month

If customers owe you more and more, you're financing their business with your cash.

Do something about it:

- Tighten payment terms: Ask for faster payment upfront.

- Collect weekly: Don't “follow up when you have time.”

- Watch aging: Old receivables are weaker than they look.

Red flag three is too much leverage

I get why founders borrow. Debt feels cleaner than giving up equity. But there's a line where useful debt becomes pressure debt.

A 2018 McKinsey analysis of 3,500 firms found that companies with debt-to-equity above 1.8 had median default rates of about 12% within 5 years, compared with 3% for those below 1.0. That gap is large enough to treat growing debt levels as a real warning, not a spreadsheet detail.

If your debt-to-equity keeps climbing, I'd do three things in order:

- Stop taking new debt to cover operating sloppiness

- Push for retained earnings by improving margin or cutting waste

- Separate growth debt from survival debt

Growth debt buys inventory that moves. Survival debt pays for yesterday's mistakes.

Red flag four is negative equity

This is the ugly one. If liabilities are greater than assets, your equity is negative. You are underwater.

When that happens, don't tell yourself a nicer story than the numbers support. Your options are usually direct:

- Put in more owner capital

- Bring in an investor

- Cut costs hard

- Raise prices if the market can take it

- Shut down weak product lines

When equity goes negative, speed matters more than elegance.

If you want a place to pressure-test these numbers with other operators who build brands, join Chicago Brandstarters. It's a free community for kind, hard-working founders in Chicago and the Midwest who want honest feedback, real tactics, and conversations that help you make better decisions before small financial problems become big ones.

Leave a Reply