You’re probably in the same spot I see all the time.

You got a quote from a supplier. You added shipping. You picked a retail price. On paper, the product looks profitable. Then cash keeps leaking out, reorders feel stressful, and every sale seems to create work instead of money.

That usually means your production cost math is fake.

I don’t mean dishonest. I mean incomplete. You counted the obvious stuff and missed the boring stuff that erodes margin: setup time, scrap, small-batch penalties, coordination across vendors, overhead that never got assigned to the product, and volume assumptions that were too optimistic.

If you want to know how to calculate production costs, stop treating it like accounting homework. Treat it like checking whether each unit is carrying its share of the load. A product that can’t carry its own weight is a liability, even if customers love it.

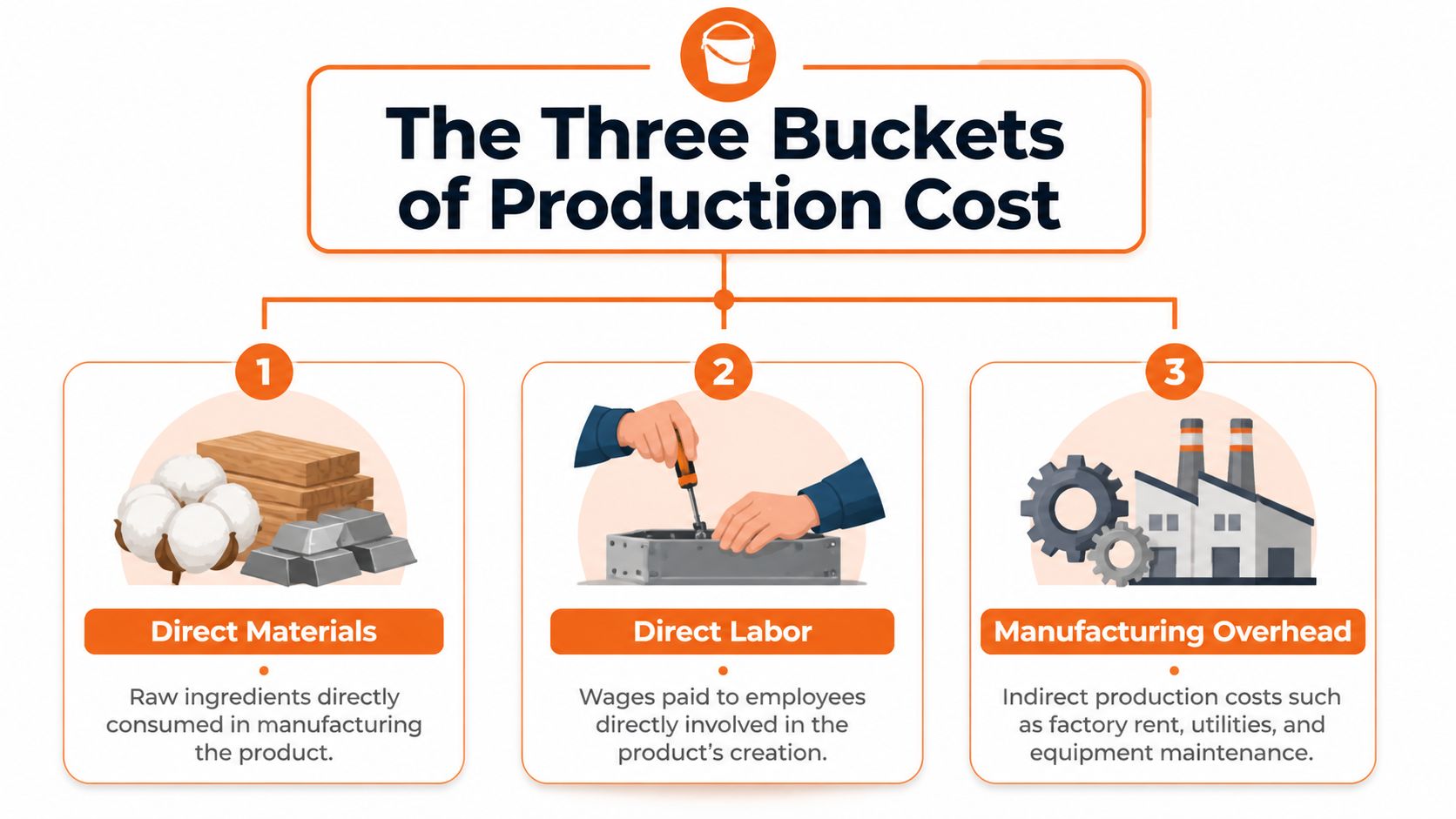

The Three Buckets of Production Cost

Most founders start with one messy spreadsheet tab called “costs.” That’s too vague. I want you to split everything into three buckets:

- Direct Materials

- Direct Labor

- Manufacturing Overhead

That’s the foundational formula: Total Production Cost = Direct Materials + Direct Labor + Manufacturing Overhead according to CFI’s production cost guide. The same source notes that in U.S. apparel, overhead often represents 20-40% of total costs, and miscalculating it is a primary reason why 30% of small manufacturing businesses fail.

Direct materials are the stuff you can touch

This bucket is the easiest one.

If you make candles, direct materials are wax, fragrance oil, jars, lids, labels, and boxes. If you make apparel, it’s fabric, thread, trims, tags, and poly bags. If the item goes into the finished product or gets consumed in making it, it usually belongs here.

The trap is acting like the supplier invoice is the whole story. It isn’t. You need your real material usage, not your ideal material usage.

Practical rule: If you need extra material because of scrap, test runs, or minimum order issues, that extra spend belongs in your product math.

If you want a second tool to sanity-check how product costs roll into margin and store profitability, I like looking at MetricMosaic for Shopify profits because it helps connect COGS thinking to actual selling economics.

Direct labor is hands-on work

This is the labor tied directly to making the unit.

That can mean sewing, filling, mixing, assembling, packing, inspecting, or labeling. If a worker spends time physically making your product, that wage belongs here. If a shop charges you per piece and that charge includes hands-on production work, treat that as direct labor or a direct conversion cost in your sheet.

A clean test helps. Ask yourself: “If I didn’t make this batch, would I still pay this cost?” If the answer is no, it’s probably direct labor or direct materials.

Overhead is where founders get sloppy

Overhead is every production cost that keeps the machine running but doesn’t belong to one specific unit. Factory rent. Utilities. Equipment maintenance. Indirect labor. Setup time that doesn’t map neatly to one item. Supervisor costs.

This bucket is the silent killer because it feels less tangible, so founders ignore it. Bad move.

Here’s the simplest way to think about it. Direct materials and direct labor are ingredients in the sandwich. Overhead is the kitchen rent, the grill cleaning, the manager, and the power bill. You still paid for the sandwich, even if you can’t see those costs stacked between the bread.

Sorting Your Costs into Fixed vs Variable Piles

Once you’ve got the three buckets, I want you to sort the same costs one more way. This time, don’t ask what the cost is. Ask how it behaves.

Use two piles:

- Fixed costs

- Variable costs

The standard formula is Total Production Cost = Fixed Costs + Variable Costs according to QuickBooks’ production cost explanation. That same source says that for an e-commerce business, variable costs can often make up 60-70% of total cost, and accurate tracking matters if you want to keep a 20-30% profit margin.

The road trip analogy

Fixed costs are like your car payment and insurance. You pay them whether you drive across town or across three states.

Variable costs are like gas. The more you drive, the more you spend.

Production works the same way.

| Cost type | What it means | Common examples |

|---|---|---|

| Fixed | Stays roughly the same in the short term | Rent, equipment lease, salaried production manager |

| Variable | Changes with output | Materials, hourly labor, packaging, freight, payment processing fees |

How I sort tricky costs

Some costs look obvious. Some don’t.

- Raw materials: Variable.

- Unit packaging: Variable.

- Hourly assembly labor: Variable.

- Factory or workshop rent: Fixed.

- Equipment depreciation: Usually fixed for your monthly planning.

- Payment processing tied to each order: Variable.

- A monthly software fee for production ops: Usually fixed.

- A setup fee charged every batch: Semi-fixed in real life, but I usually assign it to the batch and spread it across those units.

That last one matters for small-batch founders. A charge can act fixed at the batch level even if your business is tiny. If your co-packer charges a setup amount every time you run production, don’t pretend it disappears. Put it into the batch cost.

If you’re still choosing between domestic factories, co-manufacturers, or job shops, this guide to finding a manufacturer for your product helps because your supplier model changes which costs stay fixed and which move with volume.

Why this split changes your decisions

Founders usually ask, “What does this cost me?” The better question is, “What happens to this cost if I produce more or less?”

That’s how you stop making bad pricing calls.

If most of your cost is variable, your unit economics are more predictable. If you have a lot of fixed production cost, then volume matters more. Low volume will punish you. Higher volume can spread those fixed costs across more units.

That’s why two products with the same selling price can behave completely differently. One makes money at small runs. The other only works if you hit volume.

Knowing the difference keeps you from mistaking “good demand” for “good margin.”

Putting It All Together to Find Your Per-Unit Cost

You place a small production run, the invoice looks manageable, and the product still loses money. That usually happens because the founder used a supplier quote as the unit cost instead of building the full number.

Your per-unit cost is the full cost to get one finished unit out of production. For a fragmented setup with a co-packer, a print shop, a finishing vendor, and a 3PL handoff, that number only works if you pull every production cost into one sheet.

The formula is still simple. Total manufacturing cost divided by finished units. Megaventory’s guide shows the basic math clearly. What matters for small-batch founders is your inputs. If those are sloppy, the formula gives you a clean lie.

Build the sheet from the product up

Start with your BOM. Treat it like an ingredient list for money.

If you sell a custom t-shirt, your BOM might include:

- Blank shirt

- Print input or transfer

- Neck label or hang tag

- Poly bag, insert, or size sticker

- Master carton or other production packaging

Keep each item on its own line. Do not throw everything into “materials.” If the printer raises transfer costs or your packaging changes after a retailer request, you need to see exactly which input moved.

Then add waste. Real production has damaged blanks, test prints, short fills, broken seals, and units you cannot sell. If you ignore that, your spreadsheet will always understate cost.

Add labor by step, not by guess

Next, map the steps required to get from raw input to finished unit. That is your routing.

For a shirt, it may be receiving, printing, curing, QC, folding, bagging, and case packing. For a packaged food brand, it may be ingredient staging, fill, seal, code date, pack-out, and palletizing.

Assign time and cost to each step that uses labor. If you do not have formal time studies, use observed batch data. Then clean it up after the run. Founders do not need perfect factory software on day one. They need numbers that get less wrong every batch.

Add overhead with one rule and stick to it

At this point, founders usually start cheating without meaning to.

Allocate production overhead using one driver that matches how work happens. If your operation is labor-heavy, use labor hours. If machine time drives output, use machine hours. If the products are simple and very similar, using units is acceptable.

Pick the method. Keep it consistent across batches. A changing overhead method makes every comparison useless.

If you want to improve the model over time, study reducing manufacturing costs through systems engineering. The point is not academic neatness. Better systems expose where time, handling, and setup costs are eating your margin.

My recommendation: for small-batch brands, include every batch setup charge, line cleaning charge, and minimum run fee in the batch total first. Then divide by the actual finished units from that run.

Here’s a quick explainer if you want to see someone walk through the logic visually.

Use a worksheet you can update in 5 minutes

Your sheet does not need to be fancy. It needs to be honest.

| Line item | Amount |

|---|---|

| Direct materials total | Sum of all BOM items plus expected waste |

| Direct labor total | Sum of labor by production step |

| Manufacturing overhead allocated | Your assigned share of production overhead |

| Total manufacturing cost | Materials + labor + overhead |

| Units produced | Sellable finished units |

| Per-unit cost | Total manufacturing cost / units produced |

One more rule. Use sellable units, not theoretical units. If 1,000 units were planned and 940 made it through production in good condition, divide by 940.

If you run multiple SKUs, do not spread shared costs evenly like peanut butter. The SKU with extra setup, hand-finishing, changeovers, special packaging, or tighter QC should carry more cost. That is the difference between a spreadsheet that helps you price correctly and one that hides the weak product.

After you have the per-unit number, connect it to pricing with this gross margin percentage guide.

Adjusting Your Math for the Real World

Textbook formulas assume stable production. Most founders don’t have that.

You’re running pre-orders, test batches, low MOQs, changing suppliers, packaging revisions, and weird gaps between forecast and reality. If you use big-factory math without adjusting for that mess, your pricing will look disciplined and still lose money.

Your forecast volume is probably wrong

This is the first place founders get punished.

Most cost guides assume you’ll make roughly what you planned to make. But Unleashed Software’s write-up on cost of production points out the exact problem early-stage founders face: when volume falls short of projections, you need to increase your overhead burden rate to avoid underpricing. Their simple example is brutal and useful. If you projected 1,000 units but only made 500, the fixed cost allocated to each unit effectively doubles.

That means your “cheap” unit cost was only cheap because your spreadsheet believed a fantasy.

Run three scenarios every time. Best case, expected case, ugly case. Price the product so the expected case works, and check that the ugly case won’t break you.

Fragmented manufacturing changes the math

A lot of modern founders don’t use one factory. They use a fabric supplier, a printer, a local finishing shop, a co-packer, and a 3PL. That setup can work well. It can also hide costs in the cracks.

Traditional models miss the hours you spend coordinating all of it. They also miss rework when one vendor’s tolerance creates problems for the next vendor. They miss MOQ penalties, split shipments, and inventory sitting in multiple places.

That’s why I don’t trust a simple “materials plus labor” quote from a fragmented supply chain. It’s incomplete by default.

Build a founder version of costing

I’d do this in one spreadsheet with scenario tabs.

- Volume tab: Show unit cost at your expected batch size and at a lower batch size.

- Supplier tab: List every vendor in the chain and every fee they charge.

- Rework tab: Capture credits, defects, remakes, and manual fixes.

- Coordination tab: Add a line for production management time if you are doing real operator work to make the batch happen.

If you want ideas for removing waste from the system side, not just hammering suppliers on price, I’d read this piece on reducing manufacturing costs through systems engineering. It fits the actual problem better than old-school factory advice.

The point is simple. Early-stage founders don’t need prettier formulas. They need formulas that survive reality.

Common Traps That Will Silently Kill Your Margin

You quote a batch, place the order, and the numbers look fine. Then cash gets tight anyway. That usually means your sheet missed a few boring costs that hit every run.

A small brand using co-packers and specialty suppliers gets hurt here faster than a big factory. Costs slip between vendors, batches come in uneven, and one bad assumption can make a decent SKU look profitable when it is not.

Trap one ignores yield and scrap

Your actual material cost is higher than your ideal BOM if you lose product during production.

Founders love costing the perfect unit. Factories and co-packers produce messy batches, not perfect units. If labels get ruined, liquid spills during filling, fabric shrinks, or a finishing step creates rejects, your sheet needs to absorb that loss. Otherwise every reorder is underpriced from day one.

Put a yield assumption directly into the spreadsheet. Do not hide it in your head.

Trap two uses peanut butter costing

Peanut butter costing spreads overhead evenly across every SKU, even when the work is clearly uneven.

That breaks fast in fragmented manufacturing. One product may need extra setup, more approvals, hand-packing, tighter QA, or more back-and-forth with suppliers. Another product runs clean with almost no supervision. If both carry the same overhead load, your easy SKU props up your difficult SKU and you will not see the problem until margin disappears.

A simple product should not pay for a complicated product’s drama.

Trap three misses the admin tax of fragmented suppliers

This is the trap traditional factory guides keep understating.

If you use a printer, a component supplier, a co-packer, and a 3PL, somebody is doing the work of stitching that chain together. Expedited emails, schedule changes, spec clarifications, carton count disputes, relabeling, sample approvals, and remake coordination all cost money. If you do that work yourself, it is still a cost. Founder time is not free just because it does not show up on an invoice.

Watch for these margin leaks:

- Coordination time: Chasing updates, confirming specs, fixing handoff mistakes

- Quality cleanup: Rework, relabeling, remakes, manual inspection

- MOQ mismatch: Buying too much inventory to satisfy one vendor in the chain

- Split logistics: Materials and finished goods moving in separate legs between partners

If you want a clean example of how small operational charges pile up outside the obvious product quote, read this piece on managing e-commerce hidden expenses.

Trap four mixes production cost with every other business expense

Keep your production sheet clean.

Do not dump ad spend, broad admin costs, or your full founder salary into unit production cost just because you want one master number. That makes pricing harder, not easier. Production cost should answer one question: what does it take to make and land this unit in inventory?

Build a second view for company overhead if you need it. Separate views lead to better decisions.

Trap five accepts vague supplier terms

A fuzzy supplier agreement turns into a bad cost sheet.

If setup fees, spoilage responsibility, minimums, lead-time penalties, and quality standards are unclear, your spreadsheet is fiction. Small-batch founders get hit hardest because one surprise fee can wreck the margin on an entire run. Clean terms protect your math. This guide on how to negotiate with suppliers is a good place to start if your vendors keep charging you for surprises.

The fix is simple. Cost the batch you are going to run, include the friction you already know shows up, and make each SKU carry its own weight.

Your Next Move Is The Most Important

If you read all this and don’t build the sheet, none of it matters.

Knowing how to calculate production costs is not some back-office habit for later. It’s how you decide whether a product deserves more inventory, a price increase, a supplier change, or a quiet death.

Do these three things today

First, build a one-page cost sheet for one SKU only.

Not your whole catalog. One SKU. Use the buckets, sort fixed and variable behavior, and calculate a real per-unit cost. One honest SKU will teach you more than a fake master spreadsheet.

Second, run a lower-volume scenario.

Your projected batch is not reality until it ships. Check what happens if output comes in below plan. If the unit cost gets ugly fast, you need either a different price, a different batch size, or a better supplier structure.

Third, tighten supplier terms.

A lot of bad unit economics start with loose vendor agreements, unclear setup fees, or vague quality rules. This guide on how to negotiate with suppliers is useful if you need help pushing for cleaner pricing and fewer surprises.

Keep the rhythm simple

I’d review production costs every time one of these changes:

- Supplier pricing changes

- Batch size changes

- Packaging changes

- Labor steps change

- Defect or rework patterns show up

You do not need a giant ERP to do this well. You need honesty, consistency, and a spreadsheet you’ll update.

The founders who survive don’t always have cheaper products. They usually just know their numbers sooner.

That provides a critical edge. Many individuals wait until cash feels tight to check the math. By then, the math has already been wrong for months.

If you’re building a product brand and want honest feedback from operators who’ve been through supplier issues, pricing mistakes, and messy first production runs, Chicago Brandstarters has a free founder community built around small dinners and candid support for Chicago and Midwest builders.

Leave a Reply