You launch your store. A few orders trickle in. Then one lands from another state and your brain does that annoying founder thing where it skips celebration and goes straight to risk.

“Do I need to collect tax there?”

I remember that feeling. You're trying to build product, fix your landing page, chase inventory, answer customers, and now a state you've never set foot in might want paperwork from you. It feels absurd at first. It also feels like one more game built for big companies with finance teams and against scrappy operators doing everything themselves.

That reaction is normal. The taxation of electronic commerce is messy, but it's not random once you know the handful of rules that matter. You do not need to become a tax lawyer. You do need a working founder's model so you know when to ignore the noise, when to act, and when to spend money on software instead of hoping the problem stays small.

I'm going to give you the version I wish someone had given me early on. Plain English. Clear risk calls. No corporate fluff.

That First Out-of-State Sale and the Tax Panic

Your first out-of-state sale feels like proof that the brand has legs. Then it feels like a trap.

A founder I know had that exact moment after getting a few orders outside his home state. One was from California. Another was from Texas. He went from “people want this” to “am I already behind on taxes?” in about five minutes. He opened five tabs, read three conflicting articles, got more confused, and closed his laptop.

That's how this usually starts.

The problem isn't that the rules are impossible. The problem is that the internet dumps enterprise-level tax language on a solo founder who just wants to know one thing: Do I need to do anything right now?

Most of the time, the honest answer is no, not yet. One out-of-state sale usually doesn't mean instant chaos. But it is the moment when you need a system instead of vibes.

Practical rule: Don't treat tax like a fire alarm. Treat it like a dashboard. You don't need panic. You need visibility.

Here's the founder version of the truth:

- Your home state matters first. If you're operating there, you usually deal with that state before worrying about the rest.

- Out-of-state sales matter later, not never. They become a tax issue when your activity in a state gets big enough under that state's rules.

- Marketplaces and your own site are not the same. Amazon, Etsy, and eBay can remove work from your plate for marketplace sales, but your Shopify or WooCommerce store is still your problem.

If you ignore taxes completely, you're gambling. If you obsess over every possible rule on day one, you're wasting time. The sweet spot is simple. Watch your sales by state. Know your triggers. Use software before the mess gets expensive.

That's the whole game.

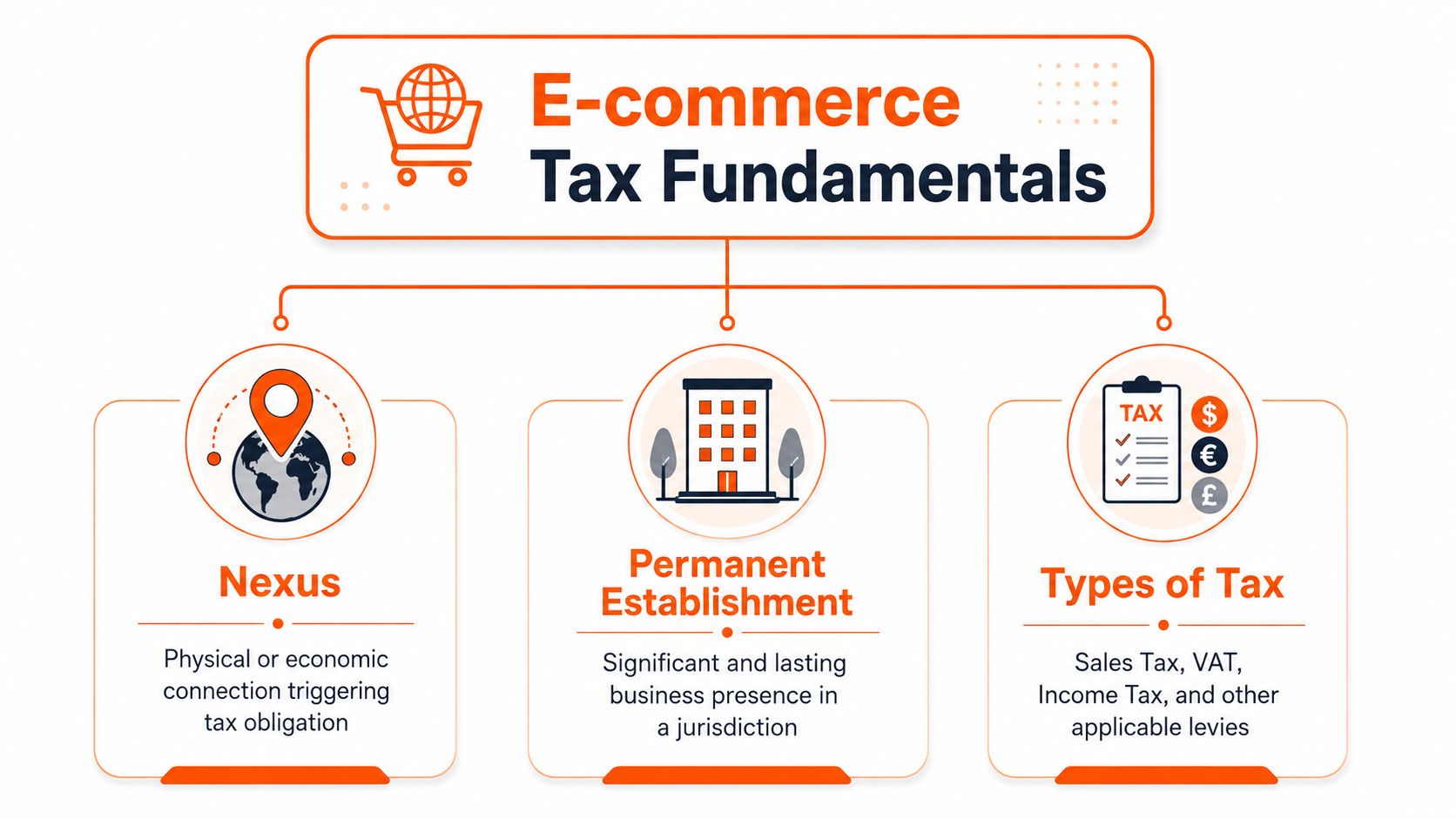

Understanding Core E-commerce Tax Concepts

Before you spend another hour reading tax content, lock in three ideas: nexus, permanent establishment, and the type of tax you're dealing with.

If you mix these up, every article on taxation of electronic commerce will sound harder than it is.

Nexus is your connection to a place

Nexus is the state saying, “You're doing enough business here that you need to follow our tax rules.”

Consider a farmers market. If you show up once as a guest vendor, nobody cares much. If you keep selling there and your booth gets busy every weekend, the organizer starts saying, “You need to register and play by the same rules as everyone else.”

That's nexus. It can come from physical presence, or from enough sales activity.

For founders, this matters because tax doesn't start everywhere at once. It starts where your business activity becomes meaningful under that state's rules. That's why sales by state reporting is so important. If you can't see where your orders are going, you can't see the problem forming.

Good financial visibility makes this easier. I like resources that explain the operational side, not just the bookkeeping side. Snyp's guide to ecommerce financial health is useful because it ties clean numbers back to actual decisions.

Permanent establishment is the international version of a real foothold

When you sell across borders, you'll hear Permanent Establishment, usually shortened to PE. This is mostly about income tax, not the same thing as US sales tax.

Think of nexus as renting a stall at the market often enough that the market cares. Think of PE as opening an actual shop in that town. You now have a real, lasting business presence there.

Under OECD-style tax rules, your business profits are typically taxable in another country only if you have a PE there, and the OECD has said that a server by itself does not automatically create a PE because it lacks the needed human intervention, as explained in this overview of electronic commerce taxation and permanent establishment.

That distinction matters for digital founders. A website reaching customers in another country is not the same thing as building a taxable business base there.

If you sell internationally, don't assume “website traffic from a country” means “income tax due in that country.” Those are different ideas.

The type of tax changes the question

A lot of founder confusion comes from saying “tax” like it's one thing. It isn't.

You're usually dealing with one of these:

- Sales tax: Common for US online sellers. You collect it from the customer and remit it when required.

- VAT: Common outside the US. It's a different system and often hits earlier in the customer transaction.

- Income tax: This is about your profits, not checkout tax.

- Other business taxes: These can show up based on product type, jurisdiction, or business structure.

Your income statement becomes way easier to read when you know what money is yours and what money you're just collecting on behalf of a government. If that distinction still feels fuzzy, this walkthrough on how to format an income statement is worth a read.

Here's the simple mental model:

| Concept | Founder translation | What it changes |

|---|---|---|

| Nexus | “Do I have enough connection here?” | Whether you must register and collect |

| Permanent Establishment | “Do I have a real business base there?” | Whether another country may tax business profits |

| Type of tax | “What tax are we even talking about?” | Whether it affects checkout, profit, or filings |

If you remember nothing else, remember this: first identify where you might owe something, then identify what kind of tax it is. That order saves a lot of bad decisions.

Decoding US Sales Tax for Online Stores

The big US rule change already happened. Before South Dakota v. Wayfair in 2018, many sellers focused on physical presence. After that case, states could require online sellers to collect sales tax even without physical presence, and 45 states implemented economic nexus laws, most commonly using $100,000 in sales or 200 transactions, while California uses $500,000, according to Statista's e-commerce tax management overview.

That one ruling changed how small online stores need to think.

Economic nexus is the rule you actually track

Economic nexus means a state can pull you into its sales tax system because of your sales activity there. You don't need an office, storefront, or warehouse in that state for this to matter.

For a scrappy founder, that means your growth can create tax obligations before your business feels “big.” A burst of orders from one state can move you from “ignore it” to “register there” faster than you expect.

Here's a simple table with examples pulled from the verified data.

| State | Sales Threshold | Transaction Threshold |

|---|---|---|

| Arizona | $100,000 | Not listed in verified data |

| Arkansas | $100,000 | 200 transactions |

| California | $500,000 | Not listed in verified data |

| Colorado | $100,000 | Not listed in verified data |

| Connecticut | $100,000 | 200 transactions |

| Florida | $100,000 | Not listed in verified data |

The point of the table is not to memorize states. The point is to notice the pattern. Many states cluster around the same sales figure, but not all of them use the same transaction test. That's why founders get tripped up when they rely on broad summaries instead of checking the states where they sell.

Marketplace sales and direct sales are different animals

If you sell on Amazon or eBay, those marketplaces often handle tax collection for third-party sellers under marketplace facilitator rules. That takes real work off your plate. But don't let that lull you into false confidence.

Sales on your own site are still where founders get surprised. Your Shopify checkout doesn't magically become compliant just because Amazon is collecting on marketplace orders. Those are separate channels with separate operational headaches.

If you sell on both Amazon and your own site, keep the channels mentally split:

- Marketplace orders: The platform often handles collection and remittance for sales on its platform.

- Direct-to-consumer website orders: You need to monitor nexus, register when required, and collect correctly.

- Reporting across both: You still need clean records, because mixed-channel businesses are where confusion starts.

If you're comparing channel complexity, this breakdown of the cost of selling on Amazon is useful because it forces you to think in channel-specific economics, not blended wishful thinking.

The mistake I see most is simple. Founders assume “I sell online” is one tax workflow. It isn't. Channel matters.

Local rates are where the annoyance really lives

People talk about state sales tax like there's one clean number. In practice, rates can vary inside the state because of local layers. That's why founders who try to do this manually eventually hate their lives.

If you've ever looked up one city's total rate and then realized a nearby area differs, you've seen the issue. Something as basic as a local reference like this 2026 Naples sales tax rate shows why “just use the state rate” is lazy advice.

Software starts paying for itself, not because tax software is exciting (it isn't), but because trying to maintain jurisdiction-level accuracy by hand is the business equivalent of using a butter knife as a screwdriver. You can do it for a minute. You shouldn't build a system around it.

My advice is blunt. If your direct sales are climbing in multiple states, stop pretending a spreadsheet alone is enough.

The Global Tax Landscape for Growing Brands

The moment you start shipping internationally, tax gets weirder fast.

Domestic sales tax is already annoying. Cross-border tax adds one more layer, because now you're dealing with countries that each have their own logic, filing expectations, and ideas about what counts as taxable activity. Big companies absorb that with teams and advisors. You won't.

Big companies play a different game

This part irritates me, but founders should see it clearly. Large e-commerce companies pay, on average, three times less in corporate income tax than traditional brick-and-mortar retailers due to complex accounting strategies, according to UNI Global Union's report on e-commerce taxation.

That doesn't mean you should obsess over corporate tax engineering. It means you should stop comparing your compliance burden to theirs. They aren't playing the same sport.

You're trying to stay clean, stay fast, and avoid stepping on landmines while growing. They're optimizing global structures with specialists.

What international rules signal to a smaller brand

You'll hear terms like OECD Pillar One, digital services taxes, and permanent establishment. For most founders, the practical lesson is simpler than the jargon.

Countries want tax revenue connected to economic activity happening with their customers. That pressure keeps producing new rules and new interpretations. Even if the biggest versions of those rules target giant firms, small brands still feel the spillover because platforms, payment flows, invoicing, and compliance expectations all get tighter over time.

I treat this like weather. I don't need to control it. I do need to know if I'm walking into a storm.

Here's the founder filter I use:

- If you're only testing international demand, keep your structure simple and your records clean.

- If a country starts becoming a real revenue driver, stop treating it like an experiment and get proper tax advice for that lane.

- If you're using fulfillment, warehousing, or local entities abroad, assume tax complexity rises and verify before scale creates a mess.

Small brands get punished less by tax rates than by sloppy structure. Confusion is usually the expensive part.

Don't borrow enterprise problems too early

Founders waste time when they study tax strategies built for multinational companies before they've even nailed channel economics at home.

Your international tax job early on is not “master global tax strategy.” Your job is much narrower:

- Know where you're selling.

- Know whether your setup creates local obligations.

- Know when the volume justifies expert help.

That's it.

The taxation of electronic commerce gets noisy because every article wants to sound global and sophisticated. I'd rather give you a cleaner standard. If the market is small, keep the setup lean. If the market becomes meaningful, formalize fast. Don't wait until you've built a real sales base in a country and then discover you've treated a permanent operation like a casual test.

Your First E-commerce Tax Compliance Playbook

You do not need a giant compliance department. You need a repeatable operating rhythm.

That means checking the right reports, acting at the right time, and buying tools before the problem costs more than the tool.

![]()

Step one is visibility, not registration everywhere

A lot of founders overreact and think they need permits in every state the moment they go live. You don't.

Start by pulling a sales-by-state report from Shopify, Amazon, WooCommerce, or whatever stack you use. If you can't quickly answer “where did my last year of orders go,” fix that first. This is a reporting problem before it becomes a filing problem.

Your first checklist is simple:

- Map your home-state exposure: Know what you owe where you operate.

- Review sales by destination: Look for states where your revenue is climbing.

- Separate marketplace from direct sales: Don't blend them and assume the platform solved all of it.

Step two is deciding when to automate

For US e-commerce sellers, compliance includes registering where you have nexus, calculating real-time tax rates across over 4,000 jurisdictions, and filing returns. Non-compliance can lead to penalties of 10-25% plus interest, and post-Wayfair, automation software from companies like Avalara reduced compliance costs by 30-50% for many businesses, according to LawShelf's module on taxation in e-commerce.

That's why I push founders toward software sooner than they want. Not because software is fun, but because manual tax management gets fragile right when the business starts moving.

Tools like Avalara, TaxJar, and Anrok can do the boring work:

- Nexus tracking: They monitor where your sales are building.

- Rate calculation: They apply the right rate at checkout.

- Filing workflows: Some help with returns and remittance.

- Exemption handling: Useful if you have B2B sales and resale certificates.

If you're still tiny, a spreadsheet and quarterly review might be enough. Once multiple states are in play, software is usually cheaper than founder time plus mistake risk.

My bias: Buy the software before you need heroics. Nobody wins awards for manually wrangling tax across a growing store.

Step three is cleaning up special cases

Founders often get ambushed. They think, “I turned on tax collection, so I'm done.” You aren't.

You still need to think through edge cases like B2B exempt sales, mixed channels, and payout reconciliation. If you don't, your books get muddy and your filings drift.

Here's a useful primer if you want a broader owner-operator lens on tax moves beyond sales tax. Million Dollar Sellers tax planning tips can spark smart questions, even if your business is still smaller than the operators in that room.

And because founder pay gets tangled up with tax decisions faster than people expect, this guide on how to pay yourself from your business helps you keep owner compensation separate from sales tax obligations and general cash chaos.

A short explainer helps here:

The operating cadence I'd use

If I were helping a founder from zero through early scale, I'd keep it this plain:

- Every month, pull sales by state. Don't rely on memory.

- Watch the states where sales keep stacking. Those are your likely next obligations.

- Turn on automation before your process gets brittle. Especially if direct sales are rising.

- Store records cleanly. Registrations, certificates, filings, and marketplace settings should live in one obvious place.

- Review quarterly. Tax neglect usually starts with “I'll check later.”

That cadence is boring. Good. Boring systems beat dramatic cleanup projects.

Next Actions A Checklist for Founders

If you feel behind, fine. Most founders are. The fix is still straightforward.

States are pushing harder on remote seller taxation, even if enforcement can still be uneven. The practical point for you is simple: audit and penalty risk rises with revenue, so proactive compliance is the smart move, as discussed in this analysis of enforcement limits and the states' taxing offensive.

Do these five things this week:

- Run a sales-by-state report: Pull the last 12 months from Shopify, Amazon, or your ERP. You need destination visibility before anything else.

- Identify your top states: Outside your home state, find the top few places where customers are buying. Those are the only places worth your attention first.

- Pick one automation tool to evaluate: Look at Avalara, TaxJar, or Anrok. Don't buy blindly. Just understand how one of them fits your store.

- Check marketplace tax settings: If you sell on Amazon, Etsy, or eBay, confirm what they are collecting and remitting for marketplace orders.

- Set a quarterly calendar reminder: Tax problems get expensive when nobody owns the review.

That's enough to move from anxiety to control.

Ignore this and you're making a bet that your growth stays small, your state exposure stays invisible, and no one asks questions later. That's a bad bet. Build the habit now while your store is still manageable.

If you're a Midwest founder building from idea stage to real revenue and you want honest operator conversations instead of fake networking, check out Chicago Brandstarters. It's a place for kind, ambitious builders to trade real war stories, solve practical problems, and grow with people who get what you're carrying.

Leave a Reply