Here's a hard truth I learned early on: profit on paper means nothing if you can't pay your bills. That's the core of cash flow management. It isn’t some accounting puzzle; it’s about making sure you always have enough actual cash on hand to cover payroll, rent, inventory, and all those other costs that pop up.

For you, the small business owner, cash flow is oxygen. Without it, your business suffocates.

Why Cash Flow Feels Like Oxygen

When I built my first app, I was obsessed with my profit and loss statement. The numbers looked great! But my bank account told a completely different, and much scarier, story. I was making "profit" but had no money to pay my developers.

That’s when it clicked. Profit is like owning a beautiful, high-performance race car. Cash flow is the fuel. Without gas in the tank, that shiny car is just a very expensive lawn ornament. It’s not going anywhere.

It’s a shockingly common mistake. You get so focused on revenue and profit margins that you forget about liquidity—the cash available right now. A recent study from OnDeck found that a staggering 82% of small business failures trace back to poor cash flow management. It’s the silent killer.

And things are only getting tougher. With inflation squeezing margins, 30% of owners now say it’s their top challenge. In the US, 51% of companies are battling uneven cash flow, making it their third-biggest operational headache.

Profit vs Cash Flow: The Core Differences

It’s easy to confuse these two, but they tell very different stories about your business's health. Think of this table as your cheat sheet for understanding the distinction.

| Concept | Profit | Cash Flow |

|---|---|---|

| Measurement | Earnings minus expenses (on paper) | Actual cash moving in and out of your bank accounts |

| Timing | A snapshot, usually quarterly or annually | A real-time pulse of your business, tracked daily or weekly |

| Impact | Shows your business's potential long-term value | Determines your immediate survival and operational breathing room |

Getting this right helps you spot the blind spots in your financial story before they become full-blown crises. Profitability is the goal, but positive cash flow is what gets you there.

Why You Need to Monitor Your Cash Flow Religiously

Constantly keeping an eye on your cash isn’t about being a pessimist; it’s about being a realist.

Here’s what it does for you:

- Eliminates nasty surprises. You’ll know exactly when you can afford that new hire or that big marketing push.

- Informs your strategy. It tells you when to invest aggressively in growth and, just as importantly, when to pull back and conserve cash.

- Plugs leaks before you sink. You can spot where money is quietly draining out of your business before it becomes a major problem.

You don't need complicated software to get started. A simple log of what's coming in and what's going out is enough. I want you to start checking your cash balance daily, or at least a few times a week. This simple habit alone can be a game-changer. If you’re just starting out, my guide on starting a business with no capital shows how this kind of basic tracking builds incredible momentum from day one.

Cash flow isn’t some optional metric for your accountant to worry about. It’s the absolute life support system for your business.

I’m not here to bore you with theory. My goal is to give you a practical, no-fluff playbook for keeping the lights on, meeting payroll, and sleeping soundly at night. In the next sections, I'll walk you through exactly how to diagnose your cash situation, build a simple forecast, and pull the right levers to keep your business healthy and growing.

How to Build Your First Cash Flow Forecast

Forecasting your cash flow isn't some dark art only for CFOs. Honestly, it's more like a weather report for your money. It tells you when to expect sunshine and when you might need to grab an umbrella, giving you precious time to prepare. You don't need fancy software—a simple spreadsheet is your best friend here.

I’m going to walk you through building a 13-week cash flow forecast. Why 13 weeks? Because it gives you a full quarter’s view, which I've found is the perfect sweet spot between long-term vision and short-term, actionable steps. This is the exact tool I use with founders to get them out of their gut and into making decisions with real confidence.

Mapping Your Cash Inflows

First up, let's get a handle on all the cash you actually expect to come into the business. This is way more than just looking at your total sales numbers. You have to get granular about when that money will physically hit your bank account.

Your cash inflows will probably include a few things:

- Sales Revenue: Project your sales on a weekly basis. And be real about it. Dig into your past data, consider seasonal trends, and factor in any promos you're running. If you're an e-commerce brand, what are your average weekly sales, really?

- Invoice Payments: When are clients actually paying you? If your terms are Net 30, don't fool yourself into forecasting that cash for the day you send the invoice. I always tell founders to add a week or two to the official due date to account for the inevitable late payers. It’s just reality.

- Other Income: Got a loan coming through? Expecting a tax refund or an investor check? Slot that into the specific week you know it's landing.

This exercise is what turns an abstract idea like "profit" into tangible, spendable cash.

A forecast is just your best-educated guess. It will never be perfect, but an imperfect plan is infinitely better than flying blind. It gives you a baseline to measure against reality.

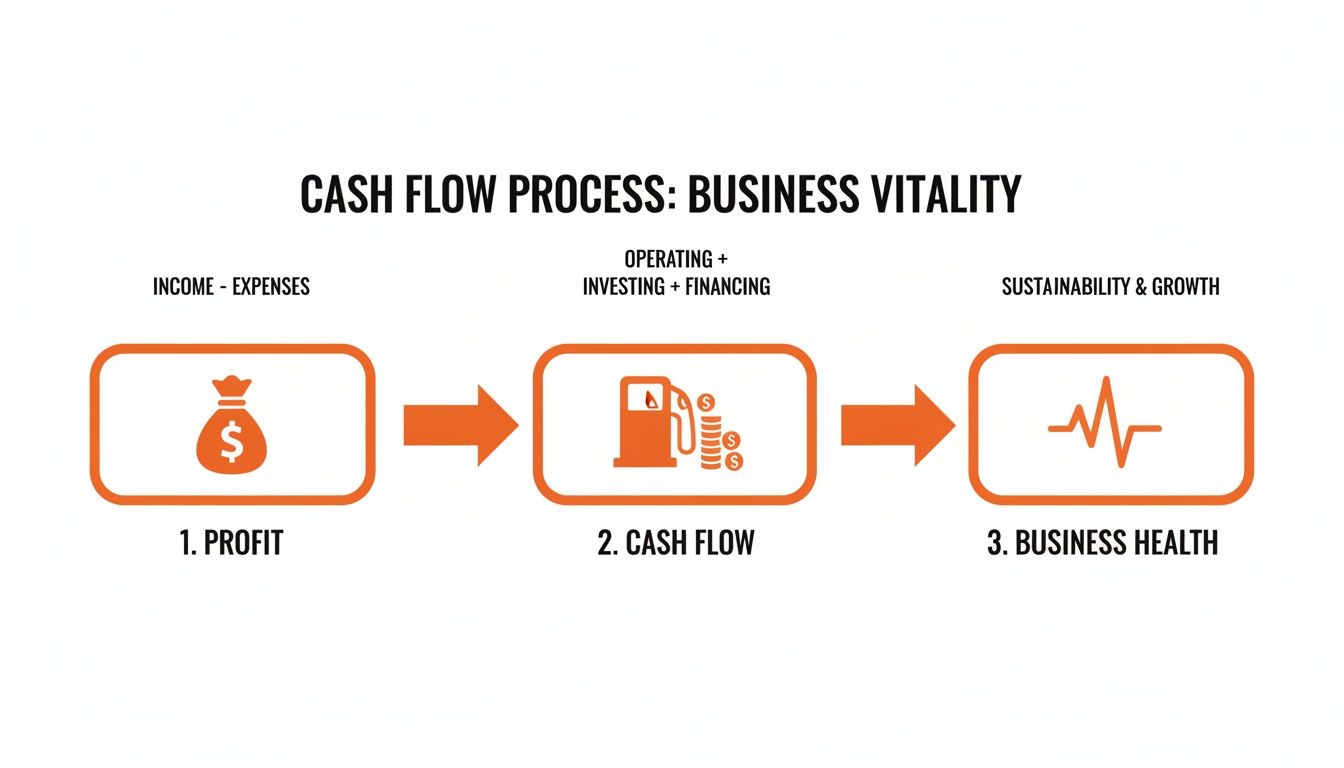

The whole point is to map the journey from a sale (which is profit on paper) to actual funds in your bank (which is cash flow). That's what really determines if your business is healthy enough to survive and grow.

This diagram nails it: profit is just the starting line. It's the cash flow that actually fuels the health and vitality of your business.

Projecting Your Cash Outflows

Now for the other side of the coin—the money going out the door. This part is usually a bit easier to pin down since so many of your costs are fixed or recurring. But you have to be brutally honest with yourself here. Underestimating your expenses is a fast track to serious trouble.

List out every single thing you have to pay for, week by week:

- Fixed Costs: These are your regulars, the predictable bills like rent, payroll, software subscriptions, and any loan payments.

- Variable Costs: These move up and down with your sales. For an e-commerce brand, think cost of goods sold (COGS), shipping fees, and what you're spending on ads.

- One-Time Expenses: Are you buying a new laptop, placing a huge inventory order, or paying that big annual insurance premium? Pinpoint the exact week that cash is scheduled to leave your account.

Putting It All Together

Okay, once you have your inflows and outflows listed out, this is where the magic happens. For each of the next 13 weeks, you’ll calculate your net cash flow (Total Inflows – Total Outflows) and, most importantly, your ending cash balance.

The math is simple:

Ending Cash = Starting Cash + Net Cash Flow for the Week

Your ending cash for Week 1 becomes the starting cash for Week 2, and so on. This rolling calculation creates a powerful snapshot of your financial future. You'll immediately spot the weeks where your bank balance might dip dangerously low, giving you a chance to do something about it before it's a five-alarm fire.

Think about it. Imagine you’re planning a big product launch. You can use this forecast to see if you can actually afford a $50,000 inventory purchase in Week 4 and still make payroll in Week 6, all based on your sales projections. That's the kind of clarity that turns chaos into control.

Shorten Your Cash Conversion Cycle

Alright, let's get tactical. Once you've built your forecast, the real work begins. Your next move is to actively shrink the time it takes to turn your investments back into real, spendable cash.

This is your Cash Conversion Cycle (CCC), and it’s one of the most powerful levers you can pull in your entire business.

Think of it this way: if you're a baker, your CCC is the time between paying for flour and a customer's payment for a cupcake actually hitting your bank account. A long cycle means your cash is trapped—in ingredients, in finished goods, or in unpaid invoices. A short cycle means you get paid faster, freeing up your capital to reinvest and grow.

The formula might look a little intimidating, but the idea is simple. You just have to manage three core parts:

- Days Inventory Outstanding (DIO): How long your products sit on the shelf before you sell them.

- Days Sales Outstanding (DSO): How long it takes your customers to pay you after a sale.

- Days Payable Outstanding (DPO): How long you take to pay your own suppliers.

Your goal is to crush your DIO and DSO, making them as short as possible, while stretching out your DPO as long as you can (without, you know, ruining your supplier relationships). Let me break down how to attack each one.

Reduce Your Days Sales Outstanding (DSO)

This is all about getting paid faster. Every day an invoice sits unpaid is another day someone else is using your money to run their business. A high DSO is an absolute cash flow killer.

I once worked with a branding agency whose DSO was a terrifying 90 days. They were profitable on paper but constantly on the brink of collapse. I helped them cut that number in half in just a few months with some simple, non-confrontational tactics.

Here’s what you can do right now:

- Invoice immediately and clearly. Don't wait until the end of the month. Send the invoice the moment the work is done with crystal-clear payment instructions and due dates.

- Offer more ways to pay. Make it ridiculously easy for people to give you money. For Chicago's bold yet kind builders, practical wins include offering payment variety to speed up inflows. Data shows 70% of businesses accept credit cards, and 62% use PayPal. You build a resilient business by making these small operational tweaks. You can find more small business cash flow insights in a report from Xero.

- Automate your follow-ups. Set up friendly, automated email reminders for invoices that are approaching their due date or are just past due. This removes the emotion and awkwardness from collections.

- Consider early payment discounts. Offering a small carrot, like 2% off if paid in 10 days instead of 30, can be a powerful nudge.

Optimize Your Days Inventory Outstanding (DIO)

If you sell a physical product, this is huge. Inventory is just cash sitting on a shelf, not working for you. Your mission is to move it as efficiently as possible.

I know a local t-shirt brand that struggled because they ordered massive batches of every design to get a lower per-unit cost. The problem? Some designs flopped, and that cash was trapped in boxes of unsold shirts for over a year.

Your inventory isn’t an asset until it sells. Before that, it’s a liability that’s actively draining your cash resources.

To shrink your DIO, you need smarter inventory management.

- Get better at forecasting. Use your past sales data to make better predictions about what will sell and when. Don't just guess.

- Try a Just-In-Time (JIT) approach. Where it makes sense, order inventory closer to when you actually need it. This reduces the time it sits in your warehouse burning a hole in your pocket.

- Liquidate slow-moving stock. Run a sale or a promotion on items that have been gathering dust. It's better to get some cash back now than no cash back ever.

Improving how you manage products on the shelf is a core part of effective cash flow management. If you want to dive deeper, my guide on the inventory turnover formula is a great place to start.

Extend Your Days Payable Outstanding (DPO)

Finally, let's talk about the money you owe. This is the one part of the cycle you actually want to make longer. By strategically timing your payments to suppliers, you keep cash in your own bank account for a longer period.

This isn't about being a deadbeat or hurting your relationships. It's about using the payment terms you've already negotiated to your advantage. If a supplier gives you Net 30 terms, don't pay the bill on day one. Pay it on day 28 or 29. That extra month of holding onto your cash can make a huge difference.

- Negotiate better terms. Once you've proven you're a reliable customer, don't be afraid to ask your key suppliers for longer payment windows, like Net 45 or even Net 60. The worst they can say is no.

- Schedule your payments. Use your accounting software or even just a calendar to schedule payments to go out right before they are due, not weeks ahead.

- Use credit cards strategically. Paying a supplier with a credit card can instantly give you an extra 30 days before the cash actually leaves your bank account. Just be sure you pay the balance in full to avoid nasty interest charges.

Proven Tactics to Get Cash in the Door Faster

Getting paid is always priority number one. But just sending an invoice and hoping for the best isn't a strategy—it's a recipe for sleepless nights. The real goal is for you to pull specific, actionable levers that get money into your bank account faster.

Think of your accounts receivable like a garden hose with a bunch of kinks in it. The water (your cash) is trying to get through, but it’s stuck. Your job is to find those kinks and straighten them out so the cash can flow freely.

Reimagine Your Invoicing and Collections

The single biggest kink for most businesses is a passive collections process. You do amazing work, send an invoice, and then… you wait. This is a massive mistake. You need to actively guide your cash home.

I worked with a founder who was constantly stressed, waiting on payments that were 60 or even 90 days past due. I helped him implement a few tiny changes that cut his average collection time by 40%. The secret? We made his invoices friendlier and his follow-up system consistent.

Here’s what you can steal from that playbook:

- Offer a Carrot: Incentivize early payments. A simple phrase like, "Pay within 10 days for a 2% discount" can work wonders. It reframes paying you early as a smart financial move for your client, not just a favor to you.

- Automate Friendly Nudges: Set up simple, automated emails. One that goes out a week before the due date as a gentle reminder, and another the day it's due. This takes the personal awkwardness out of it and ensures no invoice falls through the cracks.

- Change Your Language: I had my client ditch the sterile "Payment Due" subject line and try "Ready for Your Thoughts & Payment." It felt more collaborative and less like a demand, which, believe it or not, got a much faster response.

Don't think of collections as nagging. Think of it as excellent customer service. You're making it easy for them to do business with you and keeping their account in good standing.

Build Predictable Revenue Streams

Another powerful way to fix your cash flow is to stop living project-to-project. You have to build systems that generate predictable, recurring revenue. This is all about smoothing out those terrifying peaks and valleys.

For service businesses like mine, this means getting clients on retainers. Instead of a one-off project, you agree to a set scope of work for a fixed monthly fee. Suddenly, you have a reliable income baseline you can actually count on.

For you ecommerce founders, the principle is the same, even if the execution is a little different. The question is: how do you turn one-time buyers into repeat customers?

- Subscription Models: Can you offer your product as a monthly subscription? Think coffee, skincare, or even curated snack boxes.

- Fix Your Checkout Flow: A shocking number of sales are abandoned right at the finish line. You need to simplify your checkout, offer multiple payment options (like PayPal or Apple Pay), and be totally transparent about shipping costs upfront. Every bit of friction you remove makes it easier for cash to find its way to you.

Get Paid Before You Start the Work

This might sound like a no-brainer, but I see so many founders skip this step. For any significant project, you absolutely must require a deposit before you lift a finger. This is non-negotiable.

Requiring 30-50% upfront does two critical things. First, it immediately injects cash into your business, giving you capital to cover initial costs without draining your reserves. Second, it secures commitment. A client who has paid you a deposit is far more invested in seeing the project succeed.

Finally, I want you to take a hard look at your pricing. Sometimes the fastest path to better cash flow isn't just collecting faster—it's collecting more. Are you charging what you're truly worth? Bumping your prices by just 10% can have a massive impact on your cash reserves, often with little to no pushback from clients who already see your value.

Smart Strategies to Control Cash Outflow

Dialing in your spending is just as important as cranking up your sales. Every single dollar you don't spend is another dollar you can plow back into growth, marketing, or even your own pocket.

Being disciplined with your cash doesn't mean you have to starve your business. It just means you need to be intentional about where every dollar goes.

Think of it like packing for a long hike. You can't bring everything. You have to be ruthless about what's essential versus what's just dead weight. Let’s sort through your business’s backpack and make sure you’re only carrying what you need to get to the top.

Conduct a Ruthless Expense Review

First, you have to get an honest look at where your money is really going. Most founders I know have a decent grip on big-ticket items like rent and payroll. But it’s the small, recurring charges—the "death by a thousand cuts"—that quietly drain your bank account.

I recommend you try a simple monthly ritual. Print out your bank and credit card statements and grab three different colored highlighters.

- Green: Highlight everything that is absolutely essential to keep the lights on. This is your rent, core software, and payroll. No debates here.

- Yellow: Highlight the "nice-to-haves." These are things that are helpful but not strictly necessary for survival. Think of that extra analytics tool or the premium coffee subscription for the office.

- Red: Highlight anything that makes you ask, "What is this even for?" or "Are we still using this?" You’ll be shocked at what you find. I guarantee it.

This simple, hands-on exercise forces you to confront every single outflow. It turns your expenses from an abstract number in QuickBooks into a concrete list of decisions you’ve made. That’s powerful.

Adopt a Lean Operating Model

Especially in the early days, your default answer to any new expense should be "no." A lean mindset is your best defense against burning cash on things you don't need yet. You can always add costs later when your revenue actually justifies it.

Here are a few practical ways I’ve seen founders stay lean without slowing down:

- Freelancers Over Full-Timers: Need a great designer, writer, or bookkeeper? A skilled freelancer can deliver amazing results without the crushing overhead of a full-time salary, benefits, and payroll taxes. It’s no surprise that 38% of small businesses fail because they run out of cash; high fixed payroll costs are often the killer.

- Negotiate Everything: Never, ever accept the sticker price, especially from vendors. Whether it's your software provider or your packaging supplier, you should always ask, "Is there any flexibility on that price?" or "What do your payment terms look like?" The worst they can say is no.

- Leverage Technology Wisely: Automation is your best friend. Use tools to handle social media posting, email marketing, and even basic customer service chats. Every hour you save is an hour you can spend on things that actually bring in cash.

Your job as a founder isn't to eliminate all costs—it's to get the absolute maximum return on every single dollar you spend. Be a disciplined investor, not just a spender.

Use Your Payables Strategically

One of the most overlooked tools in your cash flow management toolbox is your accounts payable. This isn't about stiffing your vendors; it's about using the payment terms they give you to your advantage.

If a supplier gives you Net 30 terms, don't pay the invoice on day one. Pay it on day 29. That extra 28 days of holding onto your cash can be the difference between making payroll and having a full-blown panic attack. Think of it as a free, short-term loan from your supplier.

Business credit cards can also be a powerful tool, but you have to use them with extreme discipline. A card can extend your payment cycle by another 30 days, potentially giving you a 60-day buffer before cash actually leaves your account. But this is a tool for managing timing, not a lifeline to fund a failing business. You must pay that balance in full every single month, without exception.

This approach keeps your cash working for you longer. As your cash flow improves, you can start to think more about how to pay yourself from your business more consistently.

Alright, let's get down to business. All the theory in the world is useless if you don't actually do something with it. This is where you stop talking and start building. I’m giving you a straightforward 30-60-90 day plan to get a handle on your cash flow once and for all.

Think of this as your personal playbook. It's designed to take you from chaos to control, step by step.

The First 30 Days: Diagnosis Mode

Your first month is all about getting brutally honest with yourself and gaining clarity. You can't fix what you can't see, so your only goal here is to understand your financial pulse. No judgment.

- Pick your weapon. Before you do anything else, commit to a tracking system. Seriously, a simple spreadsheet is more than enough to get you started. Just list every dollar that comes in and every dollar that goes out.

- Calculate your runway. Look at your current bank balance and your average monthly burn. If your revenue dropped to zero tomorrow, how long could you keep the lights on? This number might be scary, but you need to know it.

- Track your CCC. Go ahead and calculate your Cash Conversion Cycle for the first time. The number might be ugly. That’s okay. You now have a baseline—a starting line for the race ahead.

Days 31-60: Time to Optimize

Now that you have your baseline, it's time to make a few smart moves. You’re not trying to boil the ocean here. Your goal is to find a couple of small, high-impact wins to build some momentum.

Don't overcomplicate it. Just choose one tactic to improve your cash inflows and one to tighten up your cash outflows.

- Build your forecast. This is the moment to create that 13-week cash flow forecast we talked about. Think of it as your financial weather report for the next quarter.

- Pull one "inflow" lever. As an example, start offering a 2% discount for customers who pay their invoices within 10 days. It's a simple, classic move for a reason.

- Pull one "outflow" lever. Pick one of your suppliers and just ask to extend your payment terms from Net 30 to Net 45. The worst they can say is no.

The goal here isn't perfection; it's progress. Small, consistent actions create massive change over time. Just focus on making one smart decision for your inflows and one for your outflows. That's it.

Days 61-90: Make It a System

By now, you should have much better visibility into your cash and a couple of small wins under your belt. This final month is all about turning these new actions into habits that stick. This is how you build a resilient business that can actually weather a storm.

- Schedule your weekly cash check-in. Block out 30 minutes on your calendar every single Friday. Use this time to update your forecast and review your cash position. You must treat this meeting with yourself as non-negotiable.

- Set real financial goals. Based on what your forecast is telling you, set a clear, tangible goal. Maybe it's increasing your cash runway from two months to three. Or maybe it's slashing your DSO by 15 days.

- Define your red flags. Decide now what a "cash emergency" looks like for your business. A common one is having less than 30 days of operating expenses in the bank. Figure out ahead of time what you'll do if you hit that number—will you draw on your line of credit? Cut specific costs immediately? You need to make the decision before the pressure is on.

Founder FAQs on Cash Flow Management

I get a ton of questions from founders trying to finally get a handle on their finances. It’s a common pain point, and it usually boils down to a few key worries. Here are the most common ones I hear, along with my straight-up, no-fluff answers.

What Is the Best Software When I’m Just Starting?

Honestly, don't overcomplicate this. A well-organized Google Sheet or a simple Excel spreadsheet is all you need at first.

I've seen founders waste weeks and thousands of dollars on complex software they didn't need yet. Your real goal in the beginning is to build the habit of tracking, not to become an expert in a new tool.

Once your revenue gets more consistent and you have more moving parts, then you can graduate to something like QuickBooks or Xero. For an early-stage founder like you, simple is powerful.

How Much Cash Should My Business Keep on Hand?

A solid rule of thumb is for you to have enough cash in the bank to cover at least three to six months of your essential operating expenses. Think of this as your business's emergency fund.

This is the cash you’d need for rent, payroll, and critical software subscriptions if your sales suddenly dropped to zero. This buffer gives you the breathing room to handle a slow month or an unexpected cost without panicking. If your revenue is still unpredictable, as it is for most startups, aiming for that six-month cushion is always the safer, smarter bet.

Your cash reserve isn't idle money; it's a strategic asset. It buys you time to make smart decisions instead of desperate ones.

My Cash Flow Is Always Negative. What’s the First Thing to Fix?

If you're constantly in the red, it points to a fundamental problem with your business model. The very first place you need to look is your gross margin. That's just your revenue minus the direct costs of what you sold. Are you charging enough to actually make money on each sale?

If your margins aren't healthy, you really only have two choices: raise your prices or find a way to lower your costs, period.

But what if your margins look good on paper and your bank account is still empty? Then your issue is likely your payment cycles. Are clients taking way too long to pay you? Fixing your collections process is often the quickest win for your cash flow.

At Chicago Brandstarters, I believe that kind, hardworking founders deserve to win. If you're building a brand in Chicago and want to surround yourself with a vetted community of peers who share honest war stories and real tactics, I’m here for you. Learn more and apply to join our free community at https://www.chicagobrandstarters.com.

Leave a Reply