You've done it. Your business is making money, and it's time you got paid. But you can't just pull cash out of the business account.

The right way you pay yourself is tied directly to your company's legal structure—whether you're a sole proprietorship, an LLC, or an S-Corp. If you get this wrong, you create a massive tax headache for yourself down the road. Let's make sure you get it right from the start.

Your First Paycheck The Smart Way

Figuring out how to pay yourself feels way more complicated than it should. Think of it like this: your business has its own bucket of money, and you have your personal bucket. Your job is to move money from the business bucket to yours using the correct "pipe."

The pipe you choose—an owner's draw, a salary, or a distribution—depends entirely on how you legally set up your business.

Each method has its own rules and, more importantly, tax implications. What works for a freelance designer running a sole proprietorship is totally different from what a growing e-commerce brand set up as an S-Corporation has to do. One gives you flexibility; the other demands formal payroll.

Choosing Your Payment Path

Making the right choice early on builds good financial habits and keeps you on the right side of the IRS. This is about more than just getting paid; it's about building a real, sustainable, and compliant business.

Plus, as you grow, you'll find that clean financial records are a critical step in building business credit, which opens doors for future funding and expansion.

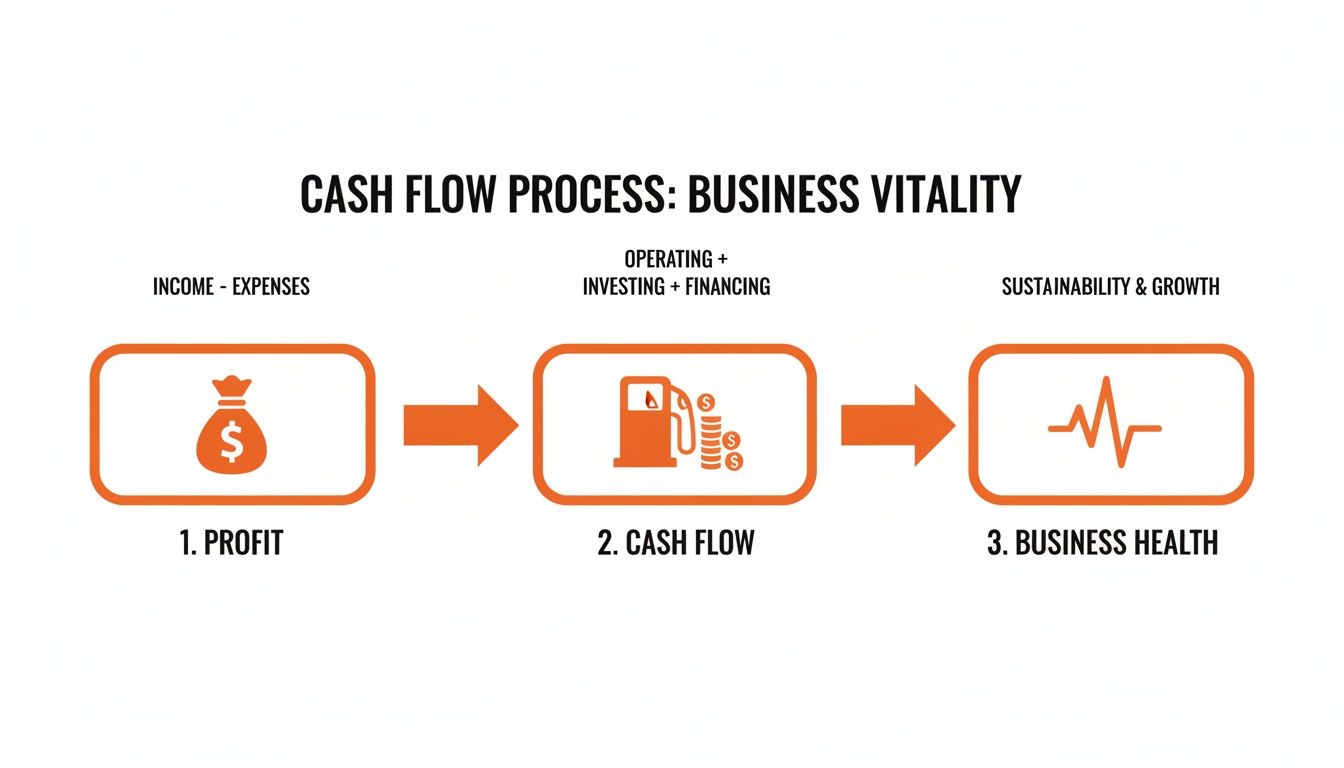

"The way you pay yourself is a direct reflection of your business's financial maturity. It’s the line that separates a hobby from a real, sustainable enterprise."

This decision tree gives you a quick visual on how your business structure dictates your payment options.

As you can see, pass-through entities like sole proprietorships and most LLCs use draws, while corporations require a formal salary. If you nail this concept, you’ve taken the first real step to mastering your business finances.

How to Pay Yourself Based on Your Business Structure

To make it even simpler, here’s a quick-reference table that breaks it all down. This chart matches the most common business types with how you're supposed to pay yourself.

| Business Entity | Primary Payment Method | How It Works | Key Tax Consideration |

|---|---|---|---|

| Sole Proprietorship | Owner's Draw | You simply transfer funds from the business account to your personal one. | No tax is withheld on the draw itself. You pay self-employment tax on all business profits. |

| Partnership | Guaranteed Payments & Draws | Partners receive guaranteed payments for services, plus draws against their share of profits. | Guaranteed payments are subject to self-employment tax. Draws are not, but profits are taxed. |

| LLC (Single-Member) | Owner's Draw | Works just like a sole proprietorship. You take money out as you need it. | Treated like a sole proprietorship. All net profit is subject to self-employment tax. |

| LLC (Multi-Member) | Guaranteed Payments & Draws | Functions like a partnership. You get paid for your work and can draw from profits. | Taxed like a partnership. Guaranteed payments are a business expense. |

| S Corporation | Salary & Distributions | You must be a W-2 employee and pay yourself a "reasonable salary" via payroll. | Your salary is subject to payroll taxes (FICA). Distributions are not, which can lead to big tax savings. |

| C Corporation | Salary & Dividends | You are an employee and must take a reasonable salary. Profits can be issued as dividends. | The business is taxed on profits, and you are taxed again on dividends (double taxation). |

This table should be your go-to guide. Pinpoint your entity type, and you’ll know exactly which payment method the IRS expects you to use.

The Core Payment Methods

Let's quickly break down the main ways you'll move that money. These are the primary tools in your financial kit.

- Owner's Draw: This is your most flexible option and the go-to for sole proprietors and single-member LLCs. You just transfer money from your business account to your personal account. No tax is withheld on the transfer, but you're on the hook for paying self-employment and income taxes on those profits when you file.

- Salary: If your business is an S-Corp or C-Corp, you're legally considered an employee. This means you must pay yourself a "reasonable salary" through a formal payroll system. Income and payroll taxes (like Social Security and Medicare) are withheld from each check, just like a regular job.

- Distribution: This is a major perk for you as an S-Corp owner. Once you've paid yourself that reasonable salary, you can take any additional profits out of the business as distributions. The magic here is that distributions are often taxed at a lower rate than your salary, which is one of the biggest advantages of the S-Corp structure.

So, How Do I Actually Pay Myself? Draws and Guaranteed Payments

If you're running a Sole Proprietorship, Partnership, or a single-member LLC, you're in luck. Getting paid is refreshingly simple. You don't have to jump through the hoops of a formal payroll system just yet. Instead, you'll use what's called an owner's draw.

Think of your business account as a dedicated piggy bank. Revenue goes in, business bills get paid from it, and when you need cash for your personal life, you take a "draw." It’s literally just a transfer from your business checking account to your personal one.

But here’s the trap that gets so many new founders into trouble: that simplicity. The money you draw isn't a "paycheck" in the traditional sense. No taxes are withheld automatically, which can lead to a nasty surprise from the IRS down the road.

The Owner's Draw, Demystified

For pass-through entities, the owner's draw is your main tool for taking money out of the business. It’s simply you claiming a piece of the company’s profits.

Imagine you're a founder in Chicago selling custom leather goods. You just crushed it this month, and after paying for leather, shipping, and ads, your business account is looking healthy. You need to pay rent, so you transfer $3,000 from your business account to your personal one. Boom. That $3,000 is your owner's draw.

You can take a draw whenever you want, for any amount, as long as the business has the cash. This flexibility is a godsend when you're starting out and revenue feels like a rollercoaster. One month you might draw $1,500; the next, maybe $5,000.

The absolute number one rule with an owner’s draw is discipline. Just because the money is sitting in the business account doesn’t mean it’s all yours. You have to leave enough cash to cover expenses, taxes, and your next big move.

A Real-World Draw Scenario

Let's stick with our Chicago leather goods founder, Sarah. She doesn't just guess what she can take. She uses a simple spreadsheet to get a clear picture of her cash flow and decide how much she can safely pay herself.

Here’s a peek at her monthly math:

| Financial Item | Amount | Notes |

|---|---|---|

| Total Monthly Revenue | $10,000 | Money coming in from all those leather bag sales. |

| Cost of Goods Sold | -$3,000 | Raw materials, direct labor, etc. |

| Operating Expenses | -$2,500 | Software, marketing, studio rent, etc. |

| Net Income (Profit) | $4,500 | What's left before her pay and taxes. |

| Tax Savings (30%) | -$1,350 | She moves this into a separate account for the IRS. Period. |

| Reinvestment Fund (10%) | -$450 | Set aside for that new sewing machine or a big marketing push. |

| Available for Owner's Draw | $2,700 | This is the maximum she can safely take this month. |

By following this framework, Sarah avoids starving her business of the cash it needs to survive and grow. She pays her future self first by carving out money for taxes and reinvestment.

What if You Have Partners? Enter Guaranteed Payments

Things get a little more complex if you have a business partner (in a Partnership or multi-member LLC). You can still take draws, but you might also introduce guaranteed payments.

Think of a guaranteed payment as a fixed salary for the actual work you do in the business, separate from your slice of the profits. It's a fair way to make sure partners who do more of the heavy lifting get compensated for it, even if the business has a slow month.

For example, you and a partner launch a marketing agency. You’re grinding away on client work and sales, while your partner is more of a silent investor. You could agree that you get a $4,000 guaranteed payment each month for your labor before any remaining profits are split. This payment is a business expense, and just like a draw, you're responsible for your own self-employment taxes on it.

Understanding the financial reality of your startup is key here. The average business startup needs about $40,000 in its first year, but that number is all over the map. A service business might launch with $12,000, while a restaurant could need $400,000 or more. For me and entrepreneurs in the Chicago Brandstarters community, knowing these numbers helps us set realistic expectations for when and how much you can actually pay yourself. You can dig into these stats further in various industry reports.

Don't Forget the Tax Man

This is the part you absolutely cannot ignore: an owner's draw is not tax-free. It's the biggest mistake I see new founders make, time and time again. You don't get taxed on the transfer of money itself, but you owe taxes on your business's entire profit for the year.

Since no taxes are being withheld, the IRS expects you to pay up throughout the year in four quarterly estimated tax payments.

- Self-Employment Tax: This covers your Social Security and Medicare. It’s a flat 15.3% on your net business income.

- Income Tax: This is your standard federal and state income tax, which depends on your tax bracket.

You have to estimate your total tax bill for the year, divide it by four, and send a payment to the IRS by their quarterly deadlines. If you fall behind, you'll get hit with painful underpayment penalties.

My best advice? Set aside 25-35% of your net income in a totally separate savings account just for taxes. Do not touch it. That's not your money—it belongs to Uncle Sam.

S-Corps: Salaries, Distributions, and How You'll Get Paid

When your business really starts to gain momentum, you might find yourself electing S-Corp status. This is a massive milestone, but it completely rewrites the rules for how you pay yourself. You're no longer just the owner taking a draw whenever you feel like it; you officially become an employee of your own company.

This shift means you have to start paying yourself a formal, W-2 reasonable salary through a real payroll system. It’s a definite move from the Wild West of flexible draws to a more structured, disciplined approach. The payoff, though? Potentially huge tax savings.

Think of your S-Corp's profit as a pie. The IRS says before you, the owner, can take any of that pie for yourself, you first have to cut a slice for the actual work you did. That first slice is your salary.

The "Reasonable Salary" Requirement

So, what exactly is a "reasonable salary"? The IRS is intentionally a bit fuzzy here, but the core idea is simple: you have to pay yourself a wage that’s comparable to what someone else would earn for doing your job in your industry and your city.

You can't just pay yourself $10,000 a year to dodge payroll taxes if you’re also acting as the CEO, top salesperson, and marketing director. That's a huge red flag.

The IRS looks at a few things to figure out if your salary is legit:

- Your Role and Responsibilities: What do you actually do all day? Are you managing a team, writing all the code, or running the entire show? The more critical your role, the higher your salary needs to be.

- Industry Averages: What do similar jobs pay in your field? You can dig up this data from places like the Bureau of Labor Statistics or even Glassdoor.

- Business Performance: Your company's revenue and profitability matter. A business pulling in $1 million in revenue can obviously support a higher owner's salary than one making $100,000.

Seriously, setting a salary that's way too low is one of the easiest ways to attract an IRS audit. They see it as a blatant attempt to avoid paying your fair share of Social Security and Medicare taxes.

The Magic of S-Corp Distributions

Okay, once you’ve paid yourself that required reasonable salary, we get to the good part: distributions.

After your salary and other business expenses are paid, any leftover profit can be taken out of the company as a distribution.

And this is where you see the tax savings kick in.

Your salary gets hit with FICA taxes—that’s the 15.3% combined tax for Social Security and Medicare. But your distributions are not subject to those FICA taxes. You’ll still owe income tax on them, but skipping that 15.3% hit can save you thousands, or even tens of thousands, of dollars every single year.

Salary Slice vs. Profit Slices

Let's say your business cleared $150,000 in profit this year. You do your research and figure out a reasonable salary for your role is $60,000. That $60,000 is the first slice of the pie, and it gets dinged with the full payroll tax.The remaining $90,000 is pure profit. You can take that $90,000 as a distribution, and you won’t pay the 15.3% FICA tax on it. That’s an instant tax savings of $13,770 compared to if you had taken the entire $150,000 as salary.

This two-part payment system—a reasonable salary followed by distributions—is the number one reason founders elect S-Corp status. It’s a powerful strategy for you to keep more of the money you earn.

Getting the Mechanics Right

Switching to an S-Corp means you can't just transfer money from business to personal anymore. You absolutely have to run formal payroll, just like you would for any other employee. This is non-negotiable.

Here’s how you do it right:

- Pick a Payroll Service: You'll need a real payroll provider. Think Gusto, Rippling, or QuickBooks Payroll. These services handle everything—calculating withholdings, filing payroll taxes, and making sure the government gets paid on time.

- Put Yourself on the Payroll: You are now a W-2 employee. You’ll get a regular paycheck (weekly, bi-weekly, whatever you choose) with all the standard deductions for income tax, Social Security, and Medicare. For many founders, this is the first time they see a "real" paystub from their own company. It's a surreal moment.

- Process Distributions Separately: When you take a distribution, it must be a completely separate transaction. This is critical. You'll make a direct transfer from your business bank account to your personal one and record it in your books as an "Owner's Distribution," not "payroll."

Keeping your salary and distributions firewalled from each other is essential for compliance. If you start mixing them up or paying your salary irregularly, you're signaling to the IRS that you’re not really treating yourself as an employee, which could undo all of your tax benefits.

And if you're thinking about the next step, like bringing on team members, check out our guide on how to hire your first employee for more practical advice.

How Much Should You Actually Pay Yourself

This is the big one, right? The question every founder I know wrestles with. It feels like walking a tightrope. On one side, you've got your personal bills and the life you're trying to build. On the other, there's the business—this living, breathing thing that needs cash to grow, survive, and not completely fall apart during a slow month.

The answer isn't "as much as I can grab." I’ve seen that movie before, and it ends in disaster.

The right number is a strategic balance between what you truly need and what the business can sustainably afford. It’s all about being brutally honest with your numbers and disciplined enough to avoid starving your business of the resources it needs to actually succeed.

Starting With Profit, Not Revenue

The single biggest mistake I see new founders make is looking at the gross revenue in their bank account and thinking it's a free-for-all. That top-line number is a vanity metric. Your real starting point for any pay discussion is your net income—your profit.

Think of your business as a fruit tree. Revenue is all the fruit it produces. But you can't just take all the fruit for yourself. You have to save some seeds for next season (reinvestment), use some to fertilize the soil (operating expenses), and set some aside for a potential drought (taxes and savings). Your pay comes from the fruit that's left over.

A game-changing framework for this is the Profit First methodology. It completely flips the standard accounting formula. Instead of Revenue - Expenses = Profit, you make it Revenue - Profit = Expenses. You decide on a profit margin first, stash that money away, and then force yourself to run the business on what's left. Your pay is a calculated part of that system, not a hopeful afterthought.

A Practical Monthly Pay Calculation

Let's make this real. Imagine you are Maria, a Chicago founder who runs a small branding agency. You had a great month and brought in $15,000. You don't just randomly Venmo yourself some cash. Instead, you follow a strict, non-negotiable allocation process.

Here’s your breakdown:

- Profit Allocation (10%): The very first thing you do is move $1,500 (10% of revenue) into a separate "Profit" savings account. This is your reward for being a smart business owner. You don't touch this money until the end of the quarter.

- Tax Allocation (25%): Next, you transfer $3,750 (25%) into your "Tax" account. This isn't your money; it belongs to the IRS and the State of Illinois. By siloing it, you avoid that horrible end-of-quarter panic when a huge tax bill comes due.

- Owner's Pay Allocation (40%): This is your paycheck bucket. You allocate $6,000 (40%) to your "Owner's Comp" account. This is the pool from which you'll pay yourself your salary or draw.

- Operating Expenses (25%): The remaining $3,750 (25%) is all you have to run the business for the next month—software, contractors, marketing, you name it. If it doesn't fit in this bucket, you can't afford it. Period.

This system forces discipline. You know exactly what you can pay yourself and what the business has left to operate. It transforms a scary, emotional decision into a simple, mathematical one.

Your business's health depends on you being its steward, not just its beneficiary. Paying yourself a sustainable amount is the ultimate act of leadership—it proves you're building something for the long haul.

Adjusting Your Pay for the Seasons

Your business is going to have good months and bad months. That's a guarantee. A rigid, fixed salary can be incredibly dangerous in the early days.

I once worked with a founder who ran an events business. His income was fantastic in the summer but cratered in the winter. He started by paying himself a high, flat salary every single month.

The first winter nearly bankrupted him. He was pulling money out of a business that wasn't making any, going into debt just to make his own "payroll."

He had to learn the hard way to be flexible. Now, he uses a percentage-based system just like Maria's. In a $20,000 summer month, his take-home pay is great. In a $5,000 winter month, it’s lean. It was a tough pill to swallow, but that discipline is why his business is still around today. He protected his cash flow management for small business, which is the absolute lifeblood of any company.

This is a critical consideration. Recent data shows the average small business owner's salary is $69,647 annually, which is about 6% higher than the national average wage. For members of the Chicago Brandstarters community growing from idea to seven figures, this provides a realistic benchmark for owner compensation during those crucial growth phases. You can find more insights about these small business statistics on Bankrate.com.

Ultimately, figuring out your pay isn't a one-time decision. It's a constant process of evaluation and adjustment. It demands you take an honest look at your numbers, commit to discipline, and adopt a mindset that prioritizes the long-term health of your business above all else.

Common Paycheck Mistakes and How to Avoid Them

One of the greatest business hacks is simply learning from other people's screw-ups. When it comes to paying yourself, a few common mistakes can create massive headaches, from surprise five-figure tax bills to serious legal trouble.

I’ve seen these exact landmines take down promising founders. The good news is, with a little foresight, you can sidestep them completely.

The Commingling Catastrophe

The number one mistake, hands down, is mixing your business and personal finances. It’s a cardinal sin for a reason.

Think of your LLC or corporation as a suit of armor protecting your personal stuff—your home, your car, your savings. Using your business account like a personal ATM punches holes directly through that armor. This is called commingling funds, and it's how you lose your legal protection.

If your business gets sued, a lawyer can argue that you and your business are the same entity because you treat its money as your own. If a judge agrees, they can "pierce the corporate veil," and suddenly, your personal assets are on the table.

The Fix: From day one, you must open a separate business checking account. All business income goes in, and all business expenses go out. You pay yourself with a clean, documented transfer (like a draw) or a formal payroll check. No exceptions. This isn't optional.

Forgetting About Uncle Sam

The second blunder I see all the time is founders forgetting that an owner’s draw isn't tax-free cash.

When you take a draw from your sole proprietorship or LLC, no taxes are withheld automatically. I’ve seen founders take draws all year, feeling flush, only to get slammed with a tax bill they can't possibly pay come April. It’s a nightmare.

You have to remember, the IRS expects you to pay taxes on your profits throughout the year with quarterly estimated payments. This covers your income tax and the hefty 15.3% self-employment tax.

The money in your business account isn't all yours. A huge chunk of it belongs to the government. If you act like it's all yours, you're setting yourself up for disaster.

The Fix: This is simple but non-negotiable. Open a separate savings account and label it "Taxes." Every time you get paid, immediately transfer 25-35% of that revenue into the tax account. This isn't your money. Do not touch it for anything other than paying your quarterly taxes. This single habit will save you from so many sleepless nights.

Setting an Unreasonable S-Corp Salary

If you run an S-Corp, the temptation to game the system is strong. Distributions are free from payroll taxes, so some founders try to pay themselves a ridiculously low salary—like $12,000 a year—and take the rest in distributions to dodge taxes.

Bad idea.

The IRS has been dealing with this trick for decades. They see an unreasonably low salary as a massive red flag. An audit will almost certainly lead them to reclassify your distributions as salary, hitting you with a bill for all the back taxes, plus penalties and interest.

The Fix: You need to do your homework. Research what a person with your experience, in your industry, and in your geographic area would earn for the job you're doing. Document this research, and then pay yourself that "reasonable salary" through a proper payroll service. It keeps you compliant and safely off the IRS's radar.

Answering Your Top Questions About Founder Pay

When you're trying to figure out how to pay yourself, it can feel like you're lost in a maze. I get it. I’ve been there.

So, I’ve put together some of the most common questions I hear from founders. No fluff, just straight answers to give you some clarity.

Think of this as your quick-reference guide. Come back to it anytime a new question pops up.

When Is The Right Time To Start Paying Myself

The short answer? When your business is consistently profitable and your cash flow is stable. Before you hit that milestone, every single dollar needs to go back into the business to fuel your growth.

A good rule of thumb is to have at least three to six months of operating expenses tucked away in a business savings account. This buffer is crucial—it ensures you're not putting the company's survival on the line just to get a paycheck.

When you do start paying yourself, start small. Even a minor, consistent payment builds good financial discipline and proves your business model can actually support you. Never, ever pay yourself if it means going into debt or pushing back payments to your suppliers.

Do I Really Need A Separate Business Bank Account

Yes. One hundred percent. This is non-negotiable. It's the very first piece of advice I give every new founder I meet.

Mixing your personal and business money is a classic rookie mistake called "commingling funds." Trust me, it makes your bookkeeping an absolute nightmare.

But more importantly, it can "pierce the corporate veil." That’s a scary legal term which means if your LLC or corporation gets sued, your personal assets—your house, your car, your savings—could be fair game. A separate account is your financial suit of armor.

You have to open a dedicated business checking account from day one. No excuses.

What Tools Can Help Me Manage Payroll And Payments

The tools you’ll need really depend on how you're set up.

- For Draws (Sole Proprietors/LLCs): Simple bookkeeping software is your best friend here. A tool like QuickBooks or Xero is perfect for tracking those money transfers from your business account to your personal one. It keeps everything clean and organized.

- For Salaries (S-Corps/C-Corps): The moment you need to run formal payroll, you absolutely need a dedicated service. Don’t even think about doing it manually. It's a recipe for costly mistakes and IRS headaches.

Gusto is incredibly popular with startups because it’s so easy to use. Another fantastic option is Rippling, which can handle a ton of other HR stuff as you start to build a team. These tools are lifesavers that automatically handle tax withholdings and filings, keeping you compliant.

How Does My Pay Structure Change As My Business Grows

Your pay structure isn't set in stone. It will, and should, evolve as your business hits new milestones.

In the very beginning, as a Sole Proprietor or LLC, you’ll probably be using flexible owner's draws. This makes sense when your revenue is all over the place. It gives you the adaptability you need.

As you scale up and your income becomes more stable and predictable, you might transition to an S-Corp. This forces the discipline of a regular, "reasonable" salary.

Then, as you start pushing past the seven-figure mark, your salary might plateau, but your distributions (your share of the profits) will likely grow quite a bit. The key is to sit down with your accountant every single year to review your compensation. This makes sure it's optimized for your personal goals, the company's health, and your overall tax strategy.

Building a business can be a lonely journey, but it doesn’t have to be. If you're a kind, hard-working founder in the Midwest, Chicago Brandstarters is your community. We skip the awkward networking and connect you with a small, private group of peers who share real stories and support each other. Learn more and apply to join at https://www.chicagobrandstarters.com.