You’ve done the hard work. You built something real from nothing. Now for the million-dollar question: how do I actually pay myself from my own business?

This isn’t just about moving money. It’s the moment your sweat equity turns into something that can sustain you, proving your business can support its most crucial asset.

The Founder's First Real Paycheck

Paying yourself isn't a luxury; it’s a core business function. Far too many founders I know treat their own pay as an afterthought, scraping together whatever’s left. That’s a fast track to burnout.

Let's change your thinking. Your pay isn't just another expense—it's the fuel keeping the engine running. You wouldn't expect a race car to win on an empty tank, so why ask that of yourself?

Imagine your business is an ecosystem. Revenue flows in, but you must allocate it wisely. It needs to cover costs, fund growth, and—this is critical—sustain the founder. When you neglect your own financial needs, you’re starving the ecosystem at its source.

Taking this step validates your effort and helps you build a sustainable life around your company. For founders who are masters at starting from nothing, our guide on how to start a business with no money shows just how vital this financial discipline is from day one.

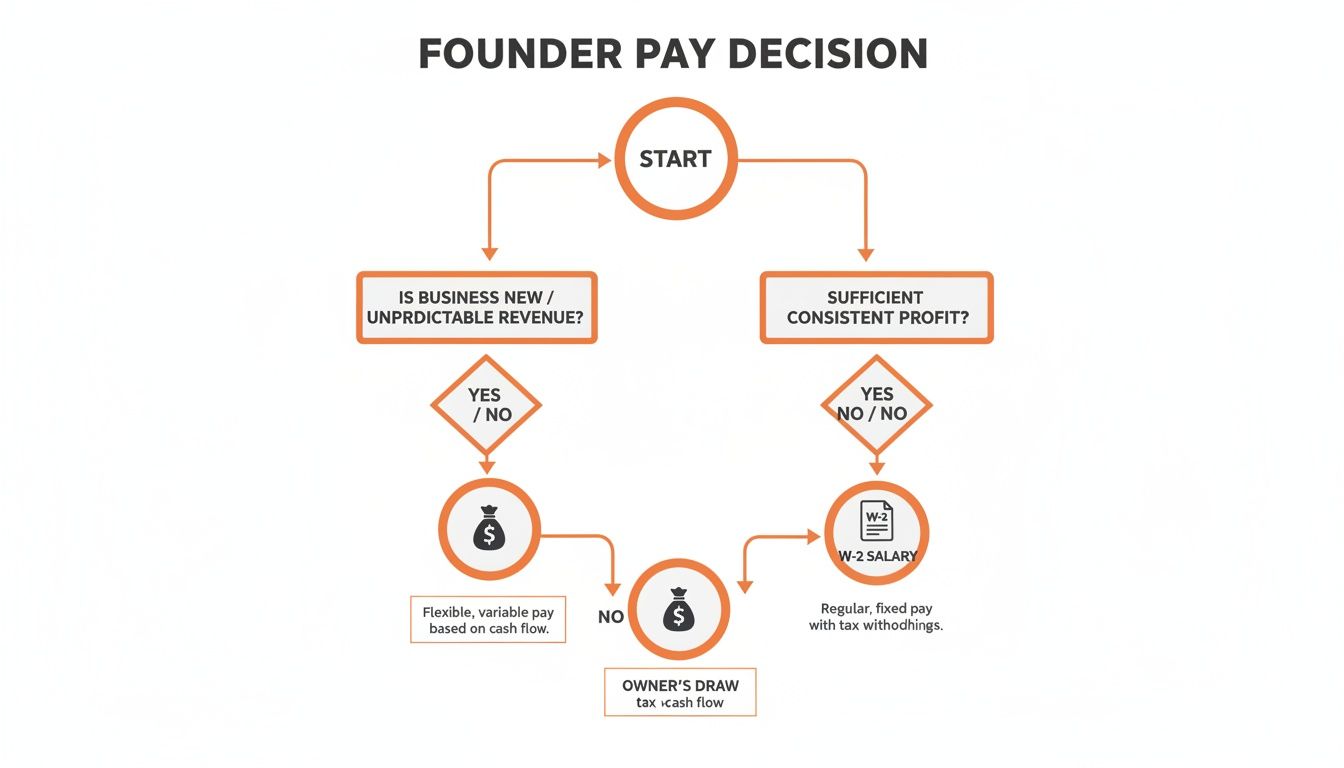

The Two Roads to Getting Paid

When it comes to the mechanics, you have two main options. Each has its own rules and tax implications, suited for different business structures.

- Owner's Draw: This is the simplest method, perfect for most sole proprietors and single-member LLCs. You just take money from business profits when you need it. It’s flexible, but you must be disciplined about setting aside money for personal taxes.

- W-2 Salary: This is the more formal route, required for corporations (including S Corps). You become an employee of your own company. You get a regular, fixed paycheck with taxes already withheld, just like any other team member.

Choosing between a draw and a salary is a strategic decision. It impacts your taxes, your personal financial stability, and even how you see your role in the company.

Getting this right from the start sets a powerful precedent. It moves you from "hobbyist" to "business owner" in a very real, tangible way.

We’ll explore how your business entity—LLC, S Corp, or something else—dictates which path you take. This will help you stay compliant and financially smart from your very first paycheck.

Matching Your Payout to Your Business Structure

Your business entity isn't just a label on a document; it’s the instruction manual for how you get paid. The path is defined by your legal structure, and picking the right one can save you thousands in taxes and countless headaches.

Think of it like choosing a vehicle. You wouldn't take a race car down a bumpy country lane. Each business structure has its own rules for the road. Get it right, and you’re cruising. Get it wrong, and you’ll find yourself stuck in serious tax mud.

Sole Proprietors and Single-Member LLCs: The Owner's Draw

For most early-stage founders, the sole proprietorship or single-member LLC is the starting line. The beauty here is its simplicity. For tax purposes, the law sees you and your business as one. You don't have to jump through payroll hoops to pay yourself.

Instead, you take an owner’s draw. It’s exactly what it sounds like—you draw money from the business profits. You can literally transfer funds from your business account to your personal one. Done. No payroll taxes are withheld.

But this simplicity comes with a huge responsibility. You are on the hook for your own taxes. This includes self-employment tax, which covers Social Security and Medicare. This is why making quarterly estimated tax payments is non-negotiable. Miss these, and you'll face nasty penalties.

Partnerships and Multi-Member LLCs: Draws and Guaranteed Payments

Things change when you bring in partners. In a partnership or multi-member LLC, owners still take draws from profits. How much each partner can pull out is spelled out in your partnership agreement—something you should have from day one.

Sometimes, a partnership might use guaranteed payments. These are fixed payments to a partner for their services, paid whether the business is profitable or not. Think of it as a pre-arranged payment, separate from splitting profits. Both draws and guaranteed payments are subject to self-employment taxes for the receiving partner.

This visual guide can help you figure out if an owner's draw or a formal salary makes more sense for where your business is now.

The key takeaway? Your revenue and profitability are the main signals telling you when to graduate from a flexible draw to a formal salary.

S Corporations: The Tax-Savvy Hybrid

For many growing businesses, electing to be taxed as an S Corporation is a game-changer. Here you move from a simple draw to a strategic hybrid approach. It’s an incredibly popular move for profitable LLCs looking to get smarter about their tax bill.

As an S Corp owner working in the business, you must pay yourself a "reasonable salary" as a W-2 employee. This salary is hit with standard payroll taxes (FICA), where the business pays its half and you pay yours. The IRS is very serious about this—your salary must align with what someone in your role and industry would earn.

The real magic of the S Corp comes after that reasonable salary. Any additional profits can be taken as distributions, and these are not subject to self-employment or FICA taxes. This is where big tax savings happen.

Let’s run a quick example:

- Business Net Profit: $120,000

- Reasonable Salary: You determine $60,000 is fair for your role. This amount gets hit with payroll taxes.

- Distributions: The remaining $60,000 can be taken as a distribution. This part is not subject to the 15.3% self-employment tax. That’s a potential tax savings of over $9,000.

Sure, this requires more admin work—running payroll and filing a separate business tax return—but the financial upside can be massive.

C Corporations: A World of Salaries and Dividends

C Corporations are completely separate legal entities. If you're an owner working for your C Corp, you are an employee. Full stop. You must be paid a W-2 salary for your work.

Here’s the catch: profits in a C Corp are taxed first at the corporate level. Then, if the corporation distributes those already-taxed profits to shareholders, it pays them as dividends. These dividends are then taxed again on your personal return.

This "double taxation" is the C Corp's defining feature. While the structure offers other benefits, especially for startups raising venture capital, it’s often the least tax-efficient for founder compensation compared to an S Corp. Your business structure fundamentally dictates your pay strategy.

Calculating a Paycheck That Sustains You and Your Business

This is where the rubber meets the road. We've covered the how, but now let's tackle the trickier question of how much. How much can you afford to pay yourself without starving your business of the cash it needs to grow?

Figuring this out feels like a high-wire act. On one side, your personal bills. On the other, the relentless demands of a growing company. Let's find that sweet spot.

Imagine your business revenue is a reservoir. Before you take water for yourself, you must account for the dam's structure (fixed costs), the town's needs (variable costs), and the water saved for a drought (taxes and reinvestment). Only then can you see what’s truly available for you.

Start with the Profit First Mindset

A powerful way to approach this is to flip the classic accounting formula. Instead of Sales - Expenses = Profit, the Profit First method suggests Sales - Profit = Expenses. This small tweak forces you to prioritize profitability and, by extension, your own pay.

You decide upfront what percentage of revenue to set aside for profit (which includes your pay). What’s left is what you have to run the business. This creates a healthy constraint, forcing you to be more resourceful.

You are the business's most critical asset. Paying yourself isn't taking from the business; it's a strategic reinvestment in its long-term stability. It’s the ultimate form of risk management.

If you don’t build your pay into the financial DNA of your business from day one, you’ll always treat it as optional. That’s a recipe for founder burnout.

The 50 Percent Rule of Thumb

So, where do you start? For many early-stage founders, a great starting point is the 50% rule. This isn't an ironclad law, but a beautifully simple guideline.

The rule suggests limiting your total owner compensation to no more than 50% of your business’s net profit (the money left after all expenses are paid).

- 50% of Profit: Goes to you as an owner's draw or salary.

- 50% of Profit: Stays in the business for taxes, reinvestment, and cash reserves.

This framework ensures you’re not draining the business account. It forces you to leave a cushion for unexpected opportunities or downturns—both are inevitable.

Grounding Your Pay in Reality

It helps to know what's normal. The reality for most founders is a long, slow climb. A whopping 86% of small U.S. business owners pay themselves under $100,000 a year, with 30% forgoing a salary entirely to reinvest everything. For solo entrepreneurs, the average dips to just $49,489 yearly.

These numbers highlight a vital strategy: resist the urge to drain your business in the early days. Set a modest, sustainable pay structure. You can dig into these small business salary benchmarks to see how you stack up.

Your compensation also reflects your pricing. If you can't pay yourself a fair wage, it might be a flashing red light that your prices are too low. Our guide on how to price a new product can help you see if your model can sustain both you and the business.

Building Your Sustainable Paycheck Plan

Alright, let's put this into an actionable plan.

- Calculate Your Personal Baseline: What’s the absolute minimum you need for essential living expenses? This is your "survival number." Don’t guess—track your personal spending for a month.

- Determine Your Business Profitability: Look at your Profit & Loss statement. What’s your average monthly net profit over the last 3-6 months? Be brutally honest.

- Apply the 50% Rule: Take your average monthly net profit and multiply it by 0.50. This is your maximum potential owner pay.

- Compare and Set Your Pay: Is the number from step 3 higher than your survival number?

- If yes: Great! You can comfortably pay yourself your baseline. Start there, then slowly increase it as profits grow.

- If no: This is a crucial signal. The business isn't profitable enough yet to fully support you. Your priority should be on increasing revenue or cutting costs, not taking a bigger draw that puts the company at risk.

This framework moves the question from "How much can I take?" to "What can the business sustainably afford to pay me?" It protects your company while ensuring you, the founder, are cared for.

Managing Taxes Without the Headaches

Taxes aren't a surprise attack; they're a predictable part of the game. Let's be real—nobody loves dealing with them, but sticking your head in the sand is a recipe for disaster. This isn’t about deciphering complex tax code; it’s tactical advice to keep you compliant without the stress.

Whether you take an owner's draw or a W-2 salary, the taxman gets his share. The key is to plan for it, not react to it. Build a system so you never have that heart-stopping moment in April when you realize you owe thousands you don't have.

Self-Employment vs. Payroll Taxes

Let's break down the two main ways you'll see taxes come out. Think of them as two roads to the same destination: paying for Social Security and Medicare.

When you take an owner's draw (common for sole proprietors and LLCs), you're on the hook for self-employment tax. This is the infamous 15.3% you’ve likely heard about. It’s made of two parts:

- 12.4% for Social Security (up to an annual income limit)

- 2.9% for Medicare (with no limit)

This feels like a huge hit because as a business owner, you foot the bill for both the "employee" and "employer" portions. In a traditional job, you'd only see half of this (7.65%) on your pay stub.

If you pay yourself a W-2 salary (required for S Corps), you're dealing with FICA taxes. The total rate is the same 15.3%, but it’s split. Your business pays 7.65% as an employer payroll tax, and you personally pay the other 7.65% through paycheck withholdings.

The bottom line is this: no matter how you pay yourself, you're contributing to these federal programs. The only difference is the mechanics of how that money gets to the government.

The Power of Quarterly Estimated Payments

Here’s the single most important habit you can build. Because taxes aren't automatically pulled from an owner's draw, the IRS expects you to pay them throughout the year in four chunks. These are your quarterly estimated tax payments.

Think of it as a payment plan for your tax bill. Instead of one massive invoice in April, you pay it down piece by piece. This prevents cash flow shocks and keeps you on the IRS's good side. Forgetting this is one of the most common—and expensive—mistakes new founders make.

Mark your calendar for these due dates:

- April 15th

- June 15th

- September 15th

- January 15th (of the next year)

How to Calculate What You Owe

Figuring out your estimated payment doesn't require an accounting Ph.D. A simple formula gets you in the right ballpark.

- Estimate Your Net Profit: Take your total business income for the quarter and subtract all legitimate business expenses. That's your net profit.

- Calculate Self-Employment Tax: Multiply that net profit by 15.3% (or 0.153). This covers Social Security and Medicare.

- Estimate Your Federal Income Tax: This is trickier since it depends on your tax bracket. A safe approach is to set aside 20-30% of your net profit for federal income tax. The right percentage depends on your total household income.

- Add Them Together: Combine your self-employment tax (step 2) and your estimated federal income tax (step 3). That's the total to set aside.

Let's use a quick example. Say your Chicago consultancy netted $20,000 in profit this quarter.

- Self-Employment Tax: $20,000 x 0.153 = $3,060

- Federal Income Tax (using a 25% estimate): $20,000 x 0.25 = $5,000

- Total Estimated Payment: $3,060 + $5,000 = $8,060

This $8,060 is what you'd send to the IRS for the quarter. Don't forget state taxes, too! Be sure to check your state's specific requirements.

Paying is the easy part. You can pay directly on the IRS website via Direct Pay or use their Electronic Federal Tax Payment System (EFTPS). The key is consistency. Every time you take a draw, immediately transfer your calculated tax portion into a separate high-yield savings account. That way, the money is ready when the due date rolls around. No stress, no surprises.

Keeping Your Business and Personal Finances Separate

If there's one non-negotiable rule, this is it: keep your business and personal finances separate. This isn't just for clean bookkeeping—it's a foundational discipline that protects you, your family, and your company's future.

Think of it like having two closets. One is for your work clothes (business account), the other for weekend gear (personal account). Mixing them creates chaos. You wouldn't show up to a client meeting in pajamas, so don't let business expenses get tangled with your grocery bill.

This separation isn’t just about staying organized for tax season. It’s about protecting your personal assets if your business faces a lawsuit. Lawyers call this the "corporate veil," and when you commingle funds, you give them a reason to pierce it. That puts your personal savings, your car, and even your home at risk.

Recording Your Pay the Right Way

How you log your pay in accounting software, like QuickBooks or Xero, is critical. An owner's draw and a salary are handled very differently on the books.

An owner's draw is not a business expense. You don't categorize it under "payroll." It’s an equity transaction. You’re simply moving money from the business's equity to your personal bank account.

In your bookkeeping, this shows up as a decrease in your Owner's Equity or Capital account. Getting this right is crucial for a true picture of your business's profitability. If you log draws as expenses, you’ll artificially deflate your profits and make bad financial decisions based on bad data.

A W-2 salary, on the other hand, is a legitimate business expense. It shows up on your Profit & Loss statement as "Payroll Expense," reducing your taxable income just like your rent.

Why This Separation Fuels Growth

Understanding your business's true financial health is everything. When your books are clean, you can answer the most important questions with confidence: Are we actually profitable? Can we afford to hire that person we need? Is it time to invest in a big inventory order?

This financial clarity is the bedrock of smart decision-making. Without it, you’re just guessing, and guessing is a terrible growth strategy.

As you build your brand, knowing these numbers helps you set smart goals for your own compensation. For instance, the average startup CEO salary recently jumped 14% to $161,000, with seed-stage CEOs averaging $147,000.

A solid benchmark for early-stage founders is to allocate 20-30% of revenue as your salary once you hit milestones like $387,000 in revenue with a small team. You can dive deeper by checking out the latest startup CEO salary report.

Keeping your finances separate is the first step to confidently paying yourself what you're worth based on real data, not a gut feeling.

Common Payout Mistakes I See All the Time

Look, every founder messes up. It’s part of the game. The smart ones learn from the blunders of others. This is about sidestepping common pitfalls that can genuinely hurt your business and your bank account.

Think of this as getting a cheat sheet from someone who has already seen what happens when you step on the landmines.

The Cash Flow Sabotage of Inconsistent Draws

One of the most tempting mistakes is treating your business bank account like a personal ATM. You pull out a big draw when sales are hot and then nothing for weeks. This wreaks havoc on your cash flow, making it impossible to forecast accurately.

The fix is simple, but it takes discipline: pay yourself on a consistent schedule, even if you're taking a draw. Pick a fixed amount on the 1st and 15th of the month. This builds stability for your personal budget and the business's financial health.

Building a predictable payout rhythm is one of the first signs of a maturing business. It forces you to operate based on real data, not the emotion of a high-revenue week.

Setting a Sketchy, Unreasonably Low S Corp Salary

If you're an S Corp, paying yourself a "reasonable salary" isn't a suggestion—it's an IRS requirement. I see this all the time: a founder sets their salary absurdly low (say, $20,000) while taking massive distributions ($200,000) to dodge payroll taxes. This is a massive red flag for the IRS.

An audit could lead to the IRS reclassifying all those distributions as salary, slamming you with back taxes, penalties, and interest. Do your homework: research what someone in your role, industry, and city would actually earn. Document it. Paying a fair salary is your best defense and a critical part of building effective small business growth strategies that protect your company.

Forgetting About Your Silent Partner: The IRS

Ignoring taxes is like ignoring a grinding noise in your car's engine; it only gets worse. For many founders, the reality of self-employment taxes hits like a ton of bricks. A stark 86% of U.S. business owners take home under $100,000 annually, with many skipping a salary entirely to fuel growth. This can create a precarious financial situation. You can see the full story on small business statistics at entrepreneurshq.com.

To avoid that gut-punch of a tax bill, here are some pro tips:

- Open a Separate Tax Savings Account. Yesterday. Every time you pay yourself, immediately slide 25-30% of that amount into a dedicated high-yield savings account. Don't touch it. It’s not your money; it’s the IRS’s.

- Use a Payroll Service Early On. Don't wait until you have a huge team. Services like Gusto or Rippling handle all payroll tax calculations and payments. It removes guesswork and saves you from costly errors.

- Review Your Pay Quarterly. Your business isn't static, and neither is your life. Every quarter, take a hard look at your profitability and personal needs. As your business grows, your compensation should evolve with it.

Answering the Tough Questions on Founder Pay

We've been there. Staring at the bank account, wondering how—and when—to finally pay yourself. These are the questions that come up time and again. Let's get right into it with some real talk.

Can I Pay Myself if My Business Isn't Profitable Yet?

This is a gut-wrenching question. The honest answer is almost always no. At least, not from profits that don't exist.

If you're pulling cash from the business before it's truly in the black, you're not getting paid. You're taking back part of your initial investment or, worse, burning through your runway from a loan or investor cash.

Look, if you absolutely need money to keep the lights on at home, the cleanest way is to structure it as a formal loan from you to the business. Get it in writing. This keeps the books clean and forces you to see the business's cash flow for what it really is.

How Often Should I Pay Myself?

Consistency is your best friend. It brings stability to your personal finances and makes business planning easier.

- For W-2 Salaries: This is easy. Get on a regular payroll schedule like everyone else. Bi-weekly or monthly are most common.

- For Owner's Draws: The flexibility here can be a trap. It's tempting to pull money out whenever you see a nice number in the business account. Don't. Set your own schedule—a fixed amount on the 1st and 15th—and stick to it. This discipline separates founders who manage their cash flow from those whose cash flow manages them.

Your pay schedule directly reflects your financial discipline. A chaotic one is a red flag for chaotic cash flow management.

What’s a “Reasonable” Salary for an S Corp Owner?

Ah, the million-dollar question from the IRS. If you own an S Corp and work in the business, you are legally required to pay yourself "reasonable compensation" before you take any tax-advantaged distributions.

But what is "reasonable"?

There's no single number. The IRS defines it as what you'd have to pay someone else with your experience and in your industry to do your job. Think of it this way: if you got hit by a bus, what would it cost to hire your replacement?

To figure this out:

- Do Your Homework: Jump on sites like Glassdoor and search for similar job titles in your city or region. What are people making?

- Document Everything: Seriously, save screenshots. Keep notes. This is your proof for the IRS if they ever ask.

Justifying your salary shows you're taking this seriously and playing by the rules. It’s one of the most important things you can do to protect yourself and the business you're building.

At Chicago Brandstarters, we believe kind, hard-working founders deserve to build sustainable businesses that support them. Join our free community to share honest war stories and get real-world advice from fellow operators who get it. Learn more and apply at https://www.chicagobrandstarters.com.